7 DeFi Trends You Must Look Out in 2026

7 mins

DeFi in 2026 is no longer defined by experiments or flashy yield. It’s defined by real capital, real users, and real infrastructure. Institutions are deploying funds onchain, stablecoins are becoming payment rails, tokenized real-world assets are finding liquidity, AI is turning into usable DeFi tooling, perps are maturing into core markets, hybrid DeFi banks are emerging, and niche protocols are building the primitives for the next decade.

In this article, we will guide you through the top 7 DeFi trends of 2026. We’ll also highlight leading projects in each trend, so read thoroughly to uncover potential gems.

DeFi Trends Defining the 2026

- Institutional Onchain DeFi

- Stablecoins

- Real-World Asset Tokenization

- AI x DeFi Tooling

- DEXs and Perpetuals

- Hybrid TradFi + DeFi

- Niche DeFi Protocols

1. Institutional Onchain DeFi Adoption Is No Longer Optional

In 2026, institutions are no longer testing DeFi at the margins. They are actively deploying capital onchain for settlement, treasury management, and lending, using stablecoins and tokenized funds as part of real operational workflows.

For years, institutional DeFi interest was framed as pilots or proofs of concept. That framing no longer fits reality.

Large financial players are now comfortable using blockchains as settlement layers.

- JPMorgan’s launch of a tokenized money market fund on Ethereum is a good example.

- BlackRock’s BUIDL Fund manages nearly $2 billion in tokenized U.S. Treasuries on Ethereum. These aren’t marketing stunts. They are infrastructure decisions.

The scale tells the story. Stablecoin transaction volumes reached roughly $27.6 trillion in 2024, already exceeding Visa’s annual volume. By late 2025, total stablecoin market capitalization passed $310 billion and continued climbing. At that point, it became hard for institutions to ignore the efficiency gains of onchain settlement.

Regulatory clarity played a major role. Frameworks like the GENIUS Act gave institutions something they could actually build against. Once compliance risk dropped, adoption accelerated quickly.

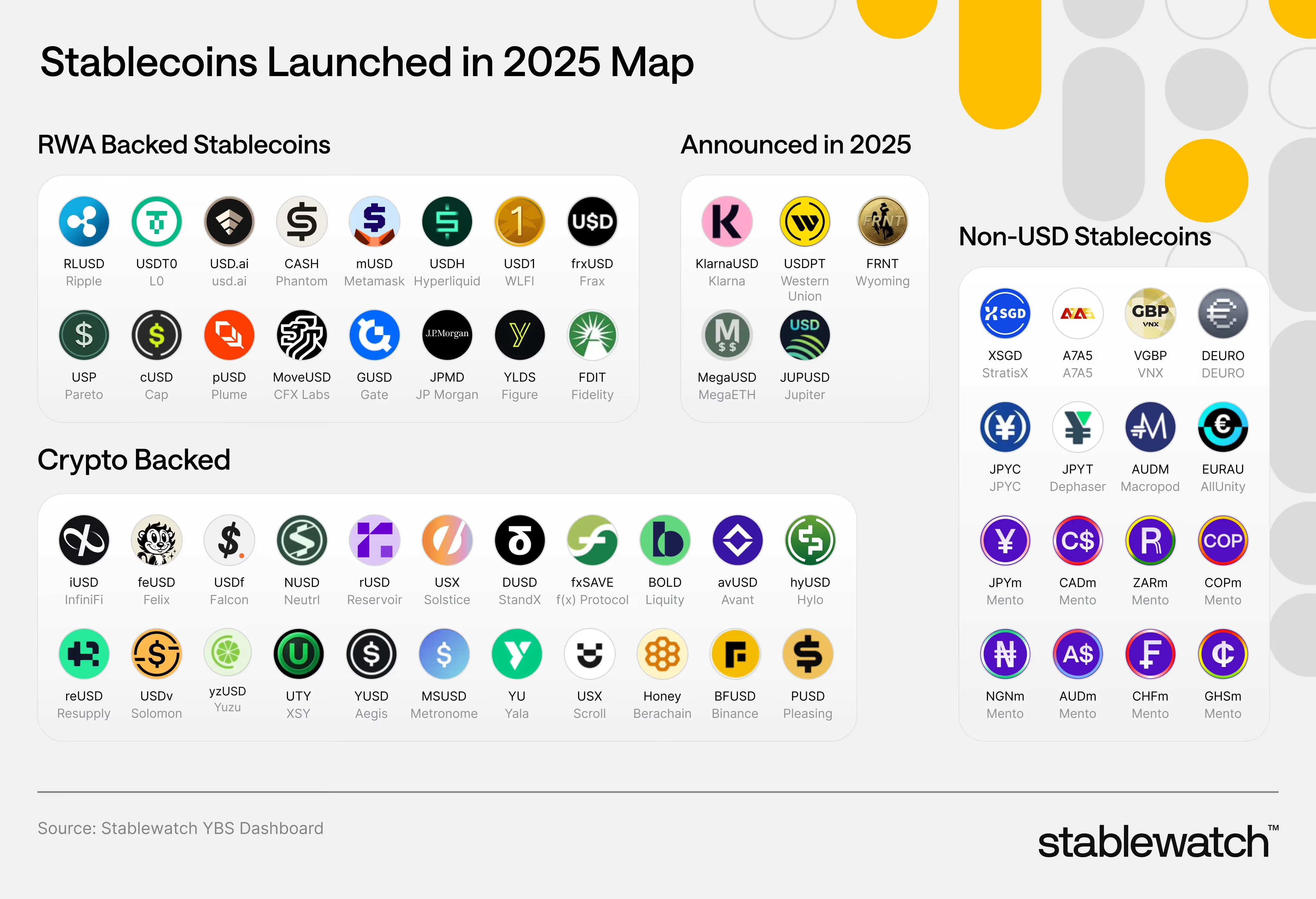

2. Stablecoins Are Becoming the Rails, Not Just the Currency

Stablecoins in 2026 are evolving from trading tools into core payment and settlement rails, increasingly used for payroll, treasury flows, cross-border payments, and institutional settlement rather than just crypto trading.

For a long time, stablecoins were treated as neutral utilities. You used them to trade, park funds, or move between exchanges. That mental model is outdated.

What’s happening now is deeper. Stablecoins are being adopted because they solve real problems that legacy systems still struggle with. They settle instantly, operate 24/7, and can be integrated directly into software workflows.

This is why Visa’s USDC settlement product matters. By late 2025, it was already running at a $3.5 billion annualized pace. Stripe’s acquisition of Bridge and issuance of USDH on Hyperliquid is another strong signal. When payment companies start building stablecoin infrastructure instead of just supporting crypto, it tells you where demand is coming from.

The most important growth is not in consumer payments yet. It’s cross-border B2B flows, corporate treasury management, and high-value settlements where speed and certainty matter more than card rewards.

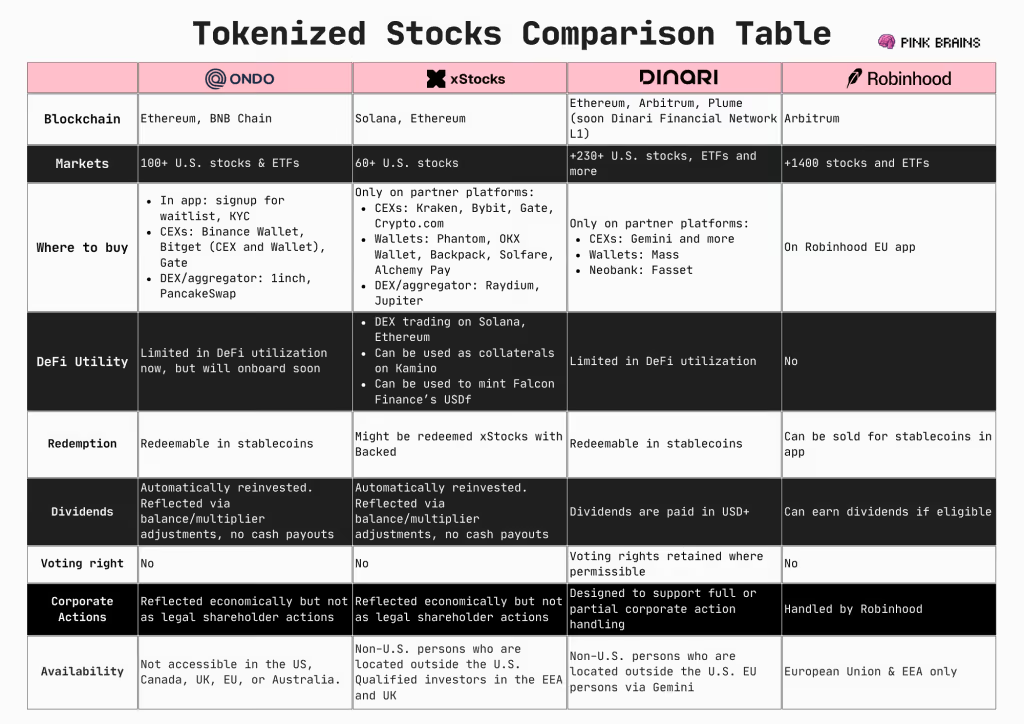

3. Real-World Asset Tokenization Is Finally Working

Real-world asset tokenization in 2026 has moved beyond theory and pilots, with equities, treasuries, commodities, and credit trading onchain at a meaningful scale and liquidity.

Growth drivers include:

- Institutional adoption is accelerating as blockchain infrastructure proves its value for 24/7 markets, instant settlement, and lower operational costs compared to legacy systems.

- Regulatory clarity in regions like the U.S., Singapore, and the EU is giving institutions the confidence to move real assets and workflows onchain.

- Growing demand for fractional ownership is expanding access to traditionally gated assets such as private equity, real estate, and private credit, pushing more value onto blockchain rails.

Tokenized RWAs now exceed $36 billion onchain, but the more important change is qualitative rather than quantitative.

- Ondo Finance illustrates this shift well. By early 2026, it had brought more than 200 tokenized U.S. stocks and ETFs to Solana and Ethereum, becoming the largest RWA issuer on the network by asset count.

- Securitize manages a large portion of U.S. tokenized treasuries, acting as a key issuer.

The takeaway is simple. Price discovery is no longer confined to traditional exchanges. It is happening onchain, around the clock, and with growing liquidity.

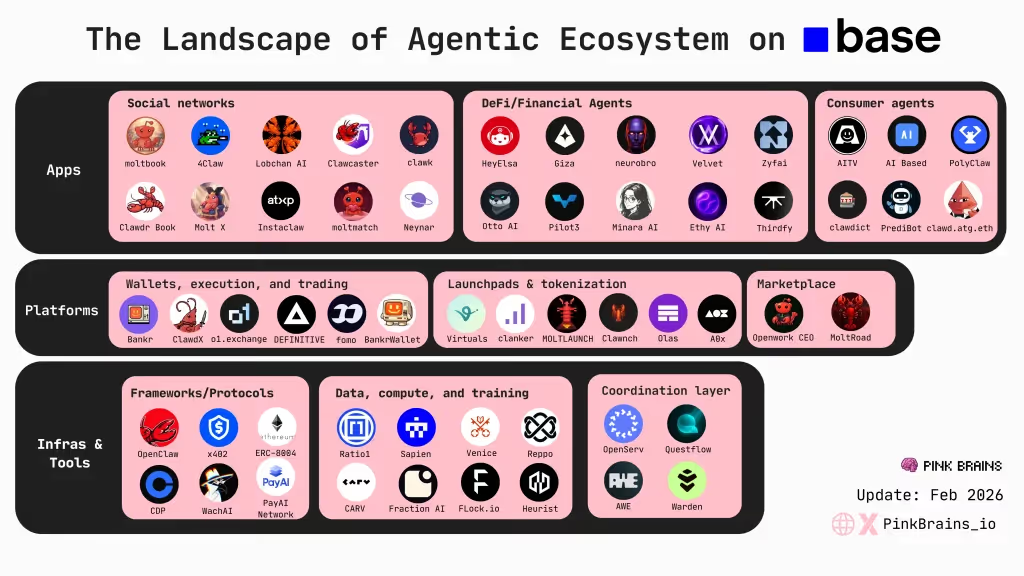

4. AI Is Becoming Practical DeFi Tooling

In 2026, AI in DeFi is moving from experimental agents to real infrastructure.

Earlier AI narratives in crypto focused on autonomous trading bots and viral demos. Most of that fell apart once real capital and risk entered the picture.

What’s different now is that AI is being treated less like a trader and more like an operator.

Two technical standards matter here.

- x402 enables native agent-to-agent payments by embedding settlement directly into API requests, allowing agents to pay for data, execution, or services without human intervention.

- ERC-8004 adds an identity and permission layer, giving agents verifiable onchain identities, reputation, and constraints. Together, they make agents accountable economic actors rather than anonymous wallets.

This infrastructure is already being used.

- Virtuals Protocol is building the coordination layer for agent economies.

- OpenClaw agents on Moltbook show how quickly agents can form social and financial behaviors once identity and payments exist. Moltbook’s launch, with hundreds of thousands of active agents in its first week, made it clear that agent-native environments are no longer theoretical.

- On the DeFi side, tools like DeFiSaver and Almanak are applying AI where it actually helps: monitoring risk, automating strategies, and assisting with capital allocation rather than chasing short-term trades.

The takeaway is simple. In 2026, AI’s real value in DeFi isn’t spectacle. It’s quietly handling payments, permissions, and coordination in systems that would otherwise be too complex for humans to manage at scale.

5. DEXs and Perpetuals Are Becoming Institutional-Grade Markets

Decentralized perpetual exchanges in 2026 are no longer niche venues. They now process trillions in volume and are increasingly competitive with centralized exchanges in liquidity, spreads, and execution quality.

Perpetual DEXs now regularly handle close to $10 billion in daily volume, with monthly volumes exceeding $1 trillion. DEXs as a whole account for more than 20% of total crypto trading, the highest share ever recorded.

- Hyperliquid is a strong example of this shift. Its onchain spreads for BTC perps are often tighter than major centralized exchanges

- Ostium opens new perpetual markets for commodities, and stocks with significant liquidity and trading volume

- New entrants like Aster and Lighter are pushing onchain orderbook design and matching engines further, narrowing the gap between centralized and decentralized execution.

Perps are no longer just speculative instruments. They are becoming foundational markets for hedging, exposure, and structured products.

6. Hybrid TradFi + DeFi Frameworks Are Going Mainstream

Hybrid frameworks that combine TradFi usability with DeFi composability are emerging as the dominant user interface for crypto, often described as DeFi banks or crypto neobanks.

Pure DeFi remains powerful, but it is still complex for most users. Pure TradFi is familiar, but extractive and closed.

Hybrid products sit in the middle. Platforms like Ether.fi, Avici, and Plasma One bundle self-custody, yield generation, borrowing, and payments into a single mobile-first experience. Users can spend stablecoins, earn yield, or borrow against positions without actively interacting with protocols or managing multiple wallets.

What makes this wave different from earlier crypto banking attempts is that these products are not just wrappers. They aggregate real DeFi primitives behind the scenes, while abstracting away complexity.

This is where adoption actually happens. Not at the protocol layer, but at the interface layer.

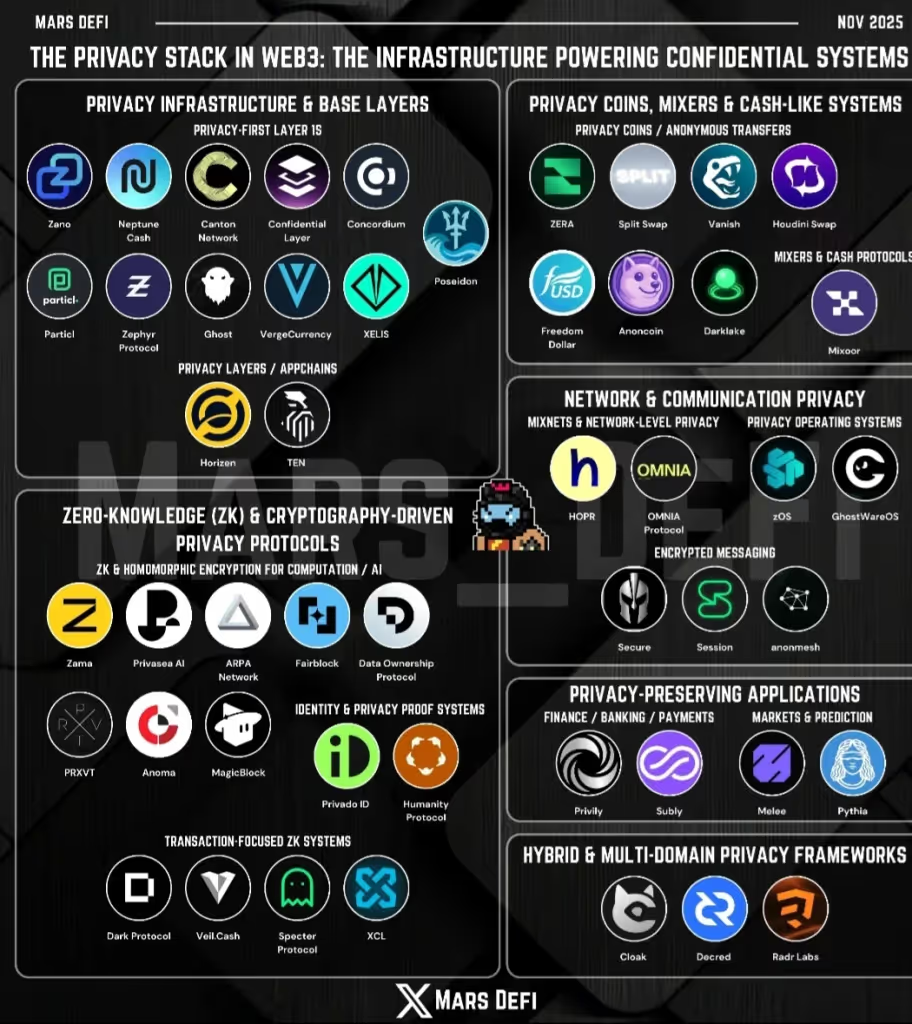

7. DeFi Protocols with Privacy as a Requirement

In 2026, the most important DeFi innovation is happening in niche protocols that combine new financial primitives with privacy-first design. Privacy is no longer optional. It is a requirement for institutional adoption and for hybrid DeFi banks to operate safely at scale.

Early DeFi assumed full transparency was always a feature. Institutions learned quickly that it breaks real strategies. Exposed balances and visible execution paths invite front-running, toxic flow, and operational risk. As a result, privacy is returning to DeFi as infrastructure, not ideology.

This is visible across the ecosystem.

- Arcium focuses on confidential computation, allowing sensitive logic and data to be processed onchain without public disclosure.

- Aztec continues to push private smart contracts, enabling shielded balances and actions while still settling on public chains.

- Starknet is used as a base layer for applications that need performance, provability, and selective privacy.

Trading infrastructure is evolving in the same direction. Paradex uses zero-knowledge systems to offer more private, non-custodial trading.

For hybrid TradFi and DeFi frameworks, this is essential. Neobanks and DeFi banks cannot expose user balances, strategies, or internal risk logic on a public ledger. Privacy-preserving execution is what allows them to offer onchain yield, lending, and trading without inheriting DeFi’s early weaknesses.

Conclusion

2026 is shaping up as a landmark year in the DeFi landscape, not with innovations but with wide adoption.

DeFi is no longer trying to prove it can exist.

It’s proving it can:

- Handle institutional capital

- Power real-world payments

- Hide complexity without hiding control

The winners in 2026 won’t be the loudest protocols.

They’ll be the ones that:

- Abstract complexity through hybrid frameworks

- Allocate capital intelligently

- Blend TradFi familiarity with DeFi sovereignty

That’s where DeFi is heading in 2026.

Disclaimer: This article serves informational purposes only and does not constitute financial advice. Conduct your own research before making investment decisions.

.png)

%201%201.png)