26 Crypto Predictions for 2026

7 mins

If you’re builders, users, and investors who want a clear understanding of where crypto is heading next year, this is a consolidated view of 26 crypto predictions for 2026, drawing from research and outlooks by Galaxy Research, a16z Crypto, Coinbase Ventures, Messari, Delphi Digital, and Bitwise.

Crypto enters 2026 in a very different place than it was just a few years ago.

Synchronized rallies or singular crypto narratives no longer define the industry. It now behaves much more like traditional markets, shaped by liquidity, distribution, and structural demand rather than speculation alone.

These are 26 crypto predictions for 2026 to watch.

Macro, Bitcoin, and Ethereum

1. Liquidity returns, but speculation does not

Global macro shifts from restriction to accommodation. Rate cuts, deficit spending, QT roll-offs, and Treasury liquidity injections rebuild the risk-on backdrop. However, capital is no longer reflexively speculative. Liquidity flows toward assets with clear ownership structures, predictable supply, and institutional legitimacy, not broad beta.

2. Structural demand separates winners from laggards

Assets outperform only when supported by durable demand. This includes ETF inflows, protocol revenue, buyback mechanisms, real user activity, and clear alignment with institutional or macro narratives. Assets without these supports struggle regardless of narrative strength.

A key 2026 dynamic is ETF flows vs. net new issuance, not just narratives. Bitwise frames that ETFs can absorb more than 100% of new supply for BTC, ETH, and SOL fit with the broader “structural bid” thesis.

3. Bitcoin breaks the four-year cycle narrative

Galaxy Research predicts that BTC will hit $250k by year-end 2027, while Bitwise expects Bitcoin to make new all-time highs in 2026. The classic “three up years then a down year” cycle weakens. The halving’s marginal impact fades, macro headwinds are likely softer, and the post-October 2025 deleveraging reduces blow-up risk. The bigger driver becomes institutional rails and allocation pathways that did not exist in prior cycles.

4. Bitcoin fully establishes itself as a macro asset

Bitcoin completes its transition into cryptomoney. It is increasingly treated as a monetary hedge alongside gold rather than a high-growth tech asset. Institutional ownership becomes structural, not opportunistic, and BTC absorbs monetary premium as weaker crypto assets lose relevance.

Bitcoin continues its slow transition from “too volatile to touch” into something institutions model like a macro allocation, not a speculative trade. A practical consequence is that Bitcoin becomes easier to hold through drawdowns inside portfolio construction, which reinforces structural demand.

5. Altcoins lose their monetary illusion

Most altcoins fail to maintain a monetary premium. As Messari highlights, declining L1 revenues expose how detached valuations have become from fundamentals. Capital increasingly treats non-BTC tokens as productive assets, not money. Tokens without cash flow, utility, or distribution compress toward zero relative to BTC.

6. Ethereum’s identity crisis resolves into infrastructure dominance

Ethereum stops competing as “digital oil” and wins as a global settlement infrastructure. It becomes the canonical layer for stablecoins, RWAs, institutional DeFi, and ZK systems. ETH accrues value indirectly through systemic importance, not direct fee capture. ETH behaves as high-beta monetary collateral to BTC, not its rival.

Stablecoins

7. Stablecoins become financial plumbing, not crypto assets

Stablecoins stop being “a crypto thing”; they are becoming the default unit of account for global digital finance. They underpin payments, FX, payroll, treasury management, lending, and agentic commerce. Issuance becomes a commodity. Competitive advantage moves to routing, liquidity access, compliance, and integration.

8. Stablechain consolidation accelerates

Many stablecoin-specific chains launch, but only a few survive. According to Delphi Digital, Arc and Tempo are not competing with Solana or Base for DeFi TVL. They are competing with SWIFT, ACH, PSPs, and internal bank settlement workflows. Their differentiator is not speed alone. It is deterministic settlement, stablecoin-denominated fees, and baked-in compliance surfaces that reduce operational friction for regulated flows.

The adoption path is productized distribution:

- Arc wins if it becomes the default rail for institutions that want Circle neutrality, deterministic finality, and auditable confidentiality.

- Tempo wins if “settle in stablecoins” becomes a Stripe-native toggle that merchants adopt without thinking about chains.

9. Onchain FX grows where TradFi is weakest

The real onchain FX opportunity lies in long-tail corridors: emerging markets, SME settlement, cross-border payroll, and B2B payments. Major FX pairs remain low-margin and competitive. Stablecoins absorb complexity where banks and legacy rails fail to serve efficiently.

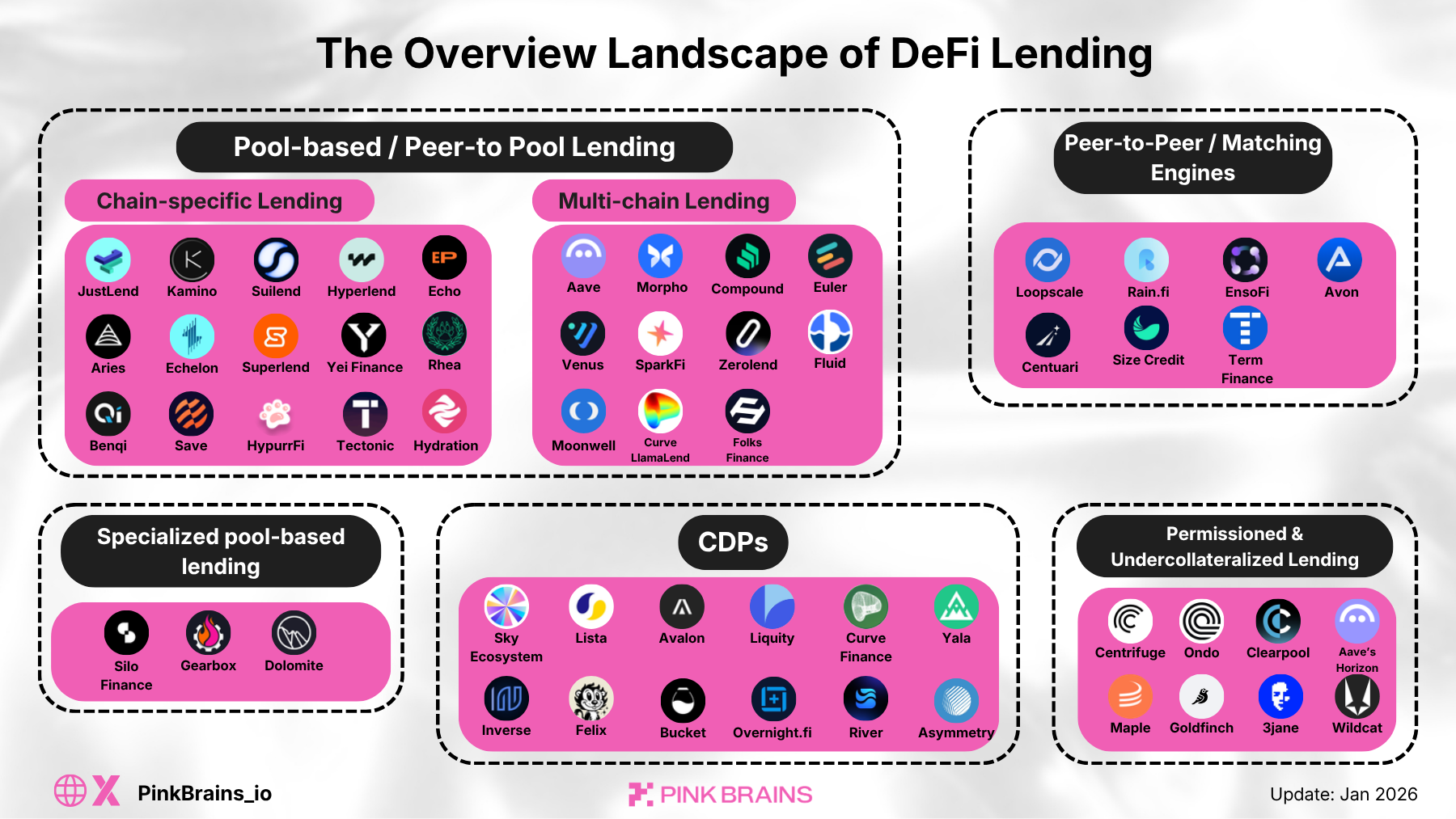

DeFi and Tokenized RWAs

10. Spot DEX architecture continues to professionalize around execution, not TVL

The most important shift Coinbase Ventures highlighted is that prop AMMs and CLOBs grow without necessarily growing TVL, because they are more capital efficient. Solana’s prop AMM arc is the clearest template:

- Liquidity is proprietary and actively quoted

- Aggregators route flow and force competition for best execution

- Oracle updates become a core microstructure primitive

- Price discovery shifts onchain for majors, not just long-tail memecoins

Expect other ecosystems to copy this once they can deliver comparable latency and cheap computation.

11. Overcollateralized credit expands, and private credit becomes DeFi’s largest real-world wedge

According to Coinbase Ventures, crypto-native lending like Aave and Morpho remains overcollateralized for core assets. However, new primitives using zkTLS, AI verification, and offchain attestations begin to unlock undercollateralized credit. Growth is incremental, not explosive, but structurally important.

Protocols specializing in institutional private credit scale faster than generalized lending, as Real-world Assets (RWAs) move beyond Treasuries into energy infrastructure, AI compute, merchant lending, and structured corporate credit. Top DeFi projects like Pendle, Maple and Centrifuge scale because they match institutional risk preferences, not because they are “DeFi.”

12. Tokenization shifts from “issuance” to “operating system”

Tokenization in 2026 is less about putting treasuries onchain and more about running a complete lifecycle: issuance, compliance, settlement, reporting, and integration into yield and collateral workflows. Mantle’s Tokenization-as-a-Service direction is an example of the platform logic.

13. Yield shifts from incentives to cash flow

Sustainable yield replaces emissions-driven yield. Yield-bearing stablecoins become default collateral, interest-rate markets deepen, and protocols without real revenue struggle to compete for capital. Yield becomes a tradeable primitive.

14. Equity perps break into mainstream usage

Perpetual DEXs remain crypto’s most successful product. Equity and index perps scale globally, especially outside the U.S without TradFi constraints. Frameworks like Hyperliquid’s HIP-3 matter because they turn listing into permissionless expansion on a liquid venue. Regulatory lag creates a window for rapid adoption before compliance frameworks catch up.

15. Hybrid CeFi-DeFi models win

Pure decentralization loses as a selling point. Pure centralization loses trust. The winners blend centralized compliance, custody, and UX with decentralized settlement and transparency. Ideology gives way to pragmatism. That's why hybrid CeFi-DeFi might become more dominant in DeFi trends 2026.

Coinbase transitions from a cyclical exchange into a financial operating system:

- Base as the execution OS

- Base App as the user interface

- USDC for settlement

- Subscriptions, x402 protocol, and derivatives as recurring revenue

The durable moat is not decentralization, but attention and trust, combined with onchain rails.

16. DeFiBanks will outcompete neobanks

A new banking model emerges: self-custodial, yield-first, globally accessible. DefiBanks offer better margins, faster settlement, and broader reach than neobanks, gradually absorbing their role without copying their structure.

17. Aggregation becomes the dominant business model

DEX aggregators, wallets, bots, and launchpads outperform base protocols economically. Aggregation compresses margins but concentrates user attention. Platforms that control the entry point capture more value than those that control liquidity.

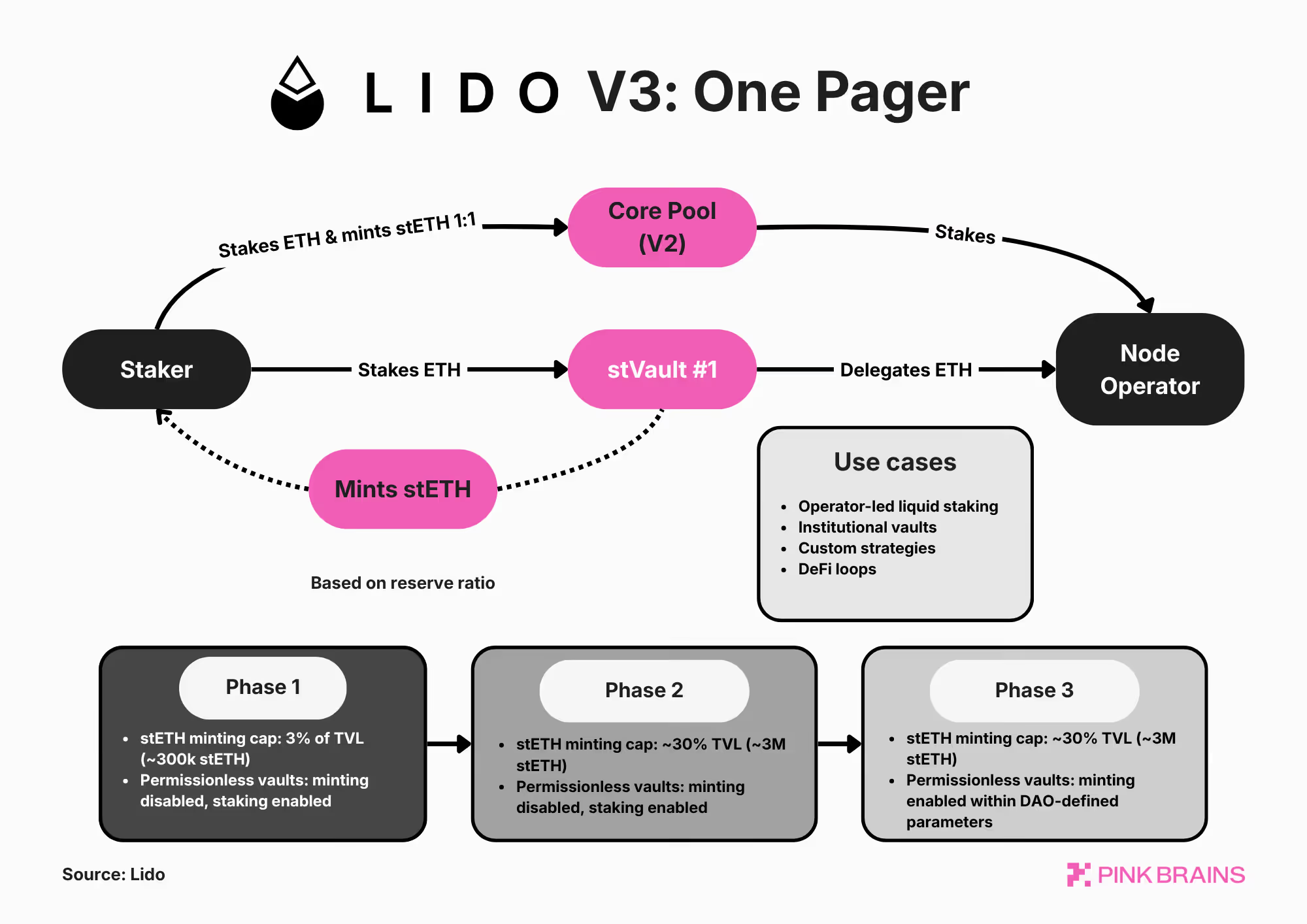

18. Onchain vaults become “ETFs 2.0” for global crypto capital

Onchain vaults like Lido’s stVaults mature into a mainstream capital allocation layer. These programmable funds allow users to deposit stablecoins while professional curators deploy capital across DeFi, RWAs, and yield strategies.

After the 2025 shakeout, 2026 becomes a quality reset:

- Weak vaults fade

- Institutional-grade curators step in

- Capital returns with a focus on risk management and cash-flow yield

As stablecoins dominate collateral and yield becomes less speculative, vaults offer diversified onchain exposure without active trading. They begin to resemble globally accessible, always-on ETFs, positioning vaults as a core interface between institutional capital and crypto-native returns.

Apps, not dApps

19. The Fat App thesis: Wallets and interfaces become high-margin businesses

Value capture shifts decisively from chains to applications. Execution layers commoditize, while apps own users, revenue, and distribution. Some L1s attempt to enshrine app revenue, but most fail to reverse the trend.

Delphi Digital predicts that crypto wallets will no longer be just storage tools but financial operating systems. Convenience, execution quality, and embedded financial services allow wallets to charge meaningful margins.

Winning platforms secure daily engagement through a strong wedge product, then expand vertically. Distribution costs collapse, UX improves, and attention becomes the scarce resource. Control the surface, control the system. Distribution, not protocol ownership, becomes the moat.

20. Platforms, not protocols, go public

Crypto IPOs accelerate. Companies with revenue, compliance, and enterprise adoption list, while most tokens fail to justify equity-like valuations. Tokens increasingly function as distribution and incentive instruments, not ownership claims.

21. Privacy becomes a baseline requirement

a16z Crypto’s analyst believed that privacy will be the most important moat in crypto. Privacy re-enters as infrastructure, not ideology. Institutions demand selective disclosure. ZK, FHE, and TEEs move into production. Privacy is embedded into wallets, protocols, and execution layers rather than isolated chains.

22. Compliance primitives move down the stack

Ripple’s XRPL or Canton Network roadmap is a clear example of where institutional chains go: native compliance and permissioning primitives rather than siloed permissioned apps. Expect more base-layer support for things like:

- Credentials gating access

- Permissioned domains

- Confidential assets with programmable disclosure

- Native lending designs that blend onchain vaults with offchain underwriting and custody constraints

The expectation is that compliance composability at the base layer unlocks more institutional volume than bespoke permissioned protocols.

23. The market becomes ruthless about value capture, and buybacks become the language of credibility

Many tokens still want to be valued like networks, but trade like inflationary incentives. The “credible token” pattern in 2026 is:

- Real revenue

- Clear sinks such as buybacks, burns, or productive staking

- A direct linkage between usage and demand

LayerZero’s Stargate, or EtherFi revenue buyback path, is the kind of mechanism investors can underwrite.

AI and Crypto

24. AI and crypto converge at the infrastructure layer

Crypto becomes the settlement, identity, and coordination layer for AI agents and embodied AI, like humanoid and robots. Compute, data, and verification markets grow, while agent-to-agent payments and reputation systems emerge. Standards like x402 and ERC-8004 enable agent payments, identity, and reputation, unlocking machine-to-machine economies.

Crypto’s role is financial and distributive, not cognitive.

25. Decentralized AI infrastructure finds PMF

Decentralized compute and data networks stop competing on ideology and start competing on cost, verification, and reliability. Verified inference, data provenance, and specialized training pipelines for small, domain-specific models succeed where they reduce cost or increase trust.

26. Prediction markets scale with AI participation

Prediction markets expand beyond election moments into sports, economics, pop culture, and business. AI participation improves calibration and liquidity. Markets become decision-support surfaces, not just betting venues.

Closing Perspective

2026 is not a hype cycle. It’s an integration cycle. Value accrues to systems that:

- own distribution

- control settlement

- capture cash flow

- embed compliance

- win daily user attention

Crypto stops asking what is possible and starts answering what actually works.

.png)

%201.svg)

%201%201.png)