Top 10 Must-Try Crypto Cards 2026: A Comparison List

9 mins

Last Tuesday, I tapped my Ether.fi card at a restaurant in Lisbon — €47 dinner, paid from my ETH collateral without selling a single wei. Two hours later, a different crypto card declined at a gas station, and I spent 20 minutes troubleshooting in Discord while the line grew behind me.

Visa-linked crypto card spending grew 525% in 2025 according to Dune Analytics. The infrastructure is real. But the headline "up to 10% cashback"? After FX fees, conversion spreads, and reward tokens that swing 40% in a week, most cards land between 1–2% effective return.

Here are the top 10 crypto cards from our test.

1. Ether.fi Cash Card

Ether.fi Cash lets you borrow against your ETH and spend stablecoins — your assets keep earning yield while you use them. Non-custodial, Visa-powered, Apple Pay and Google Pay ready. KYC cleared in about 48 hours when I tested it, and the metal card are only available in the US. The catch: my first non-USD purchase came with a ~1% FX fee that wasn't obvious in the app.

On X, the community is polarized. An user account praised EtherFi over MetaMask Card on its ecommerce 2FA approval which helps the card be more secure in using.

A feature that most crypto cards list forget to compare is ecommerce 2FA approval. This is the exact reason why @etherficard is better than @metamask card. Problem: to approve a ~$400 purchase MM card (powered by @CL_Technology) attempts to send me an SMS. But I’m in foreign country, using a travel eSIM. I can’t receive SMS in my cheap cheap Argentina phone provider. So I can’t make the purchase. Solution: The etherfi team (powered by @raincards) enabled to approve the purchase also by email 2FA, so I can easily access that from wherever I want. Source: @AriEiberman

Card Offers:

There are different tiers based on the Club membership program.

- Core: 1 free physical card, 3 virtual cards. No annual fee for the card itself (0.01 ETH Club fee). 2% cashback. $20K/day spending limit.

- Luxe: 2 free physical cards, 10 virtual cards. 0.1 ETH Club fee. 3% cashback. $150K/day spending limit.

- Pinnacle: 5 free physical cards, unlimited virtual cards. 1 ETH Club fee. 3% cashback. $1M/day limit. Includes 1 free conference per year.

- VIP: Invitation only. Includes Ether.fi Ventures Access.

During the February 2026 promotional period, all tiers received 3% cashback. The card also includes Visa Signature benefits: price protection, purchase protection, extended warranty, and rental car insurance.

Pros:

- Borrow against ETH and spend without selling — assets keep earning yield

- Up to 3% cashback (promotional campaigns have gone higher)

- Non-custodial with direct DeFi wallet integration

- Zero annual card fee; Apple Pay and Google Pay supported

- Integrated yield via UltraYield Stablecoin Vault

- Borrow Mode and Direct Pay Mode give flexibility

- You can now fund EtherFi account with stablecoins (USD, USDT) from Solana or Tron without fees

Cons

- Limited regional availability — U.S. rollout still partial, restricted in several countries

- Borrowing involves liquidation risk if collateral drops during market dips

- ~1% FX fee on non-USD transactions quietly eats into cashback

- Cashback token and promotional campaigns change frequently

- KYC delays reported by users in South America, Southeast Asia, and parts of Africa

- No traditional banking protections like FDIC insurance

Best for: DeFi-native ETH holders who want yield-while-you-spend and are comfortable managing collateral ratios. Not for beginners or anyone uncomfortable with liquidation risk.

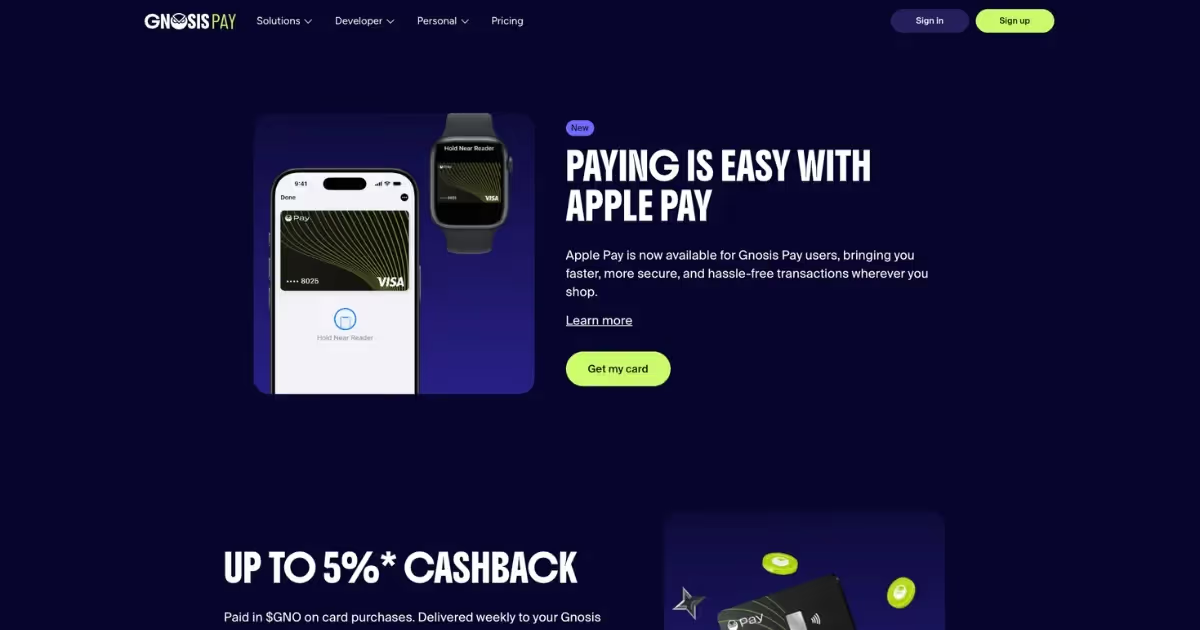

2. Gnosis Pay

Gnosis Pay connects directly to your Safe wallet on Gnosis Chain — one of the most genuinely self-custodial cards available. Bridging and Safe setup took me about 30 minutes including one failed transaction. Once configured, spending was smooth at every Visa merchant. Trustpilot sits at 2.9/5 — users flag complex activation and slow support, but praise the 0% FX model.

Cashback is tiered based on GNO token holdings in your Card Safe.

Card Offers:

- 1% cashback: Entry level, minimal GNO holdings

- 2% cashback: ~€1,000 in GNO

- 4% cashback: ~100 GNO held in Safe

- +1% bonus: OG NFT holders (max 5%)

- Cashback paid weekly in GNO tokens via airdrop

- 0% FX fees on all transactions

- €30 annual card fee

- €8,000 daily spending limit

Pros:

- Full self-custody — funds stay in your Safe wallet, not with a third party

- Up to 5% cashback (4% base + 1% OG NFT bonus) in GNO

- Zero FX fees, accepted at millions of Visa merchants worldwide

- Direct stablecoin spending — no need to off-ramp first

- Gasless transaction experience — no xDAI needed

- Developer-friendly with open smart contract infrastructure

Cons:

- Requires bridging to Gnosis Chain, which adds setup friction

- Cashback paid in GNO — a volatile token that can lose value quickly

- €30 annual fee is higher than fully free alternatives

- Balance update lag compared to centralized cards

- Trustpilot reviews flag complex activation, slow support, and KYC issues

- Only supports three stablecoins (EURe, GBPe, USDCe)

- Currently limited to EEA, UK, Argentina, and Brazil

Best For: European crypto users who prioritize decentralization over convenience and are already comfortable managing Safe wallets and on-chain assets. If you hold GNO, this is a no-brainer.

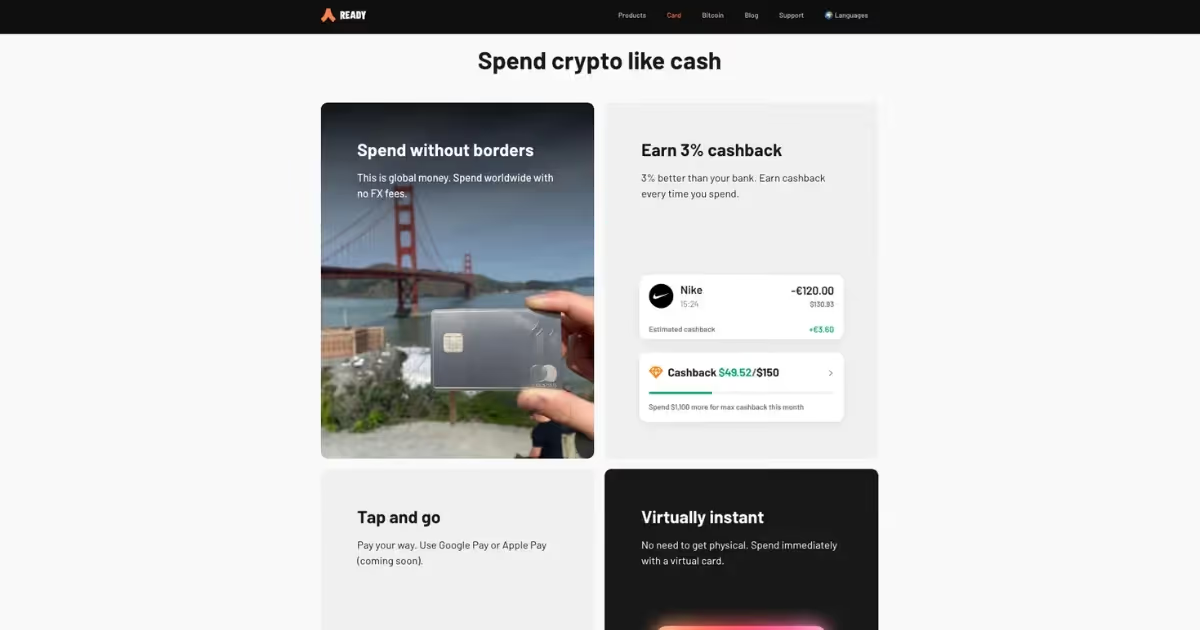

3. Ready Card

Ready (formerly Argent) is a self-custodial Mastercard built on Starknet. Your USDC stays in your own smart contract wallet until the moment you spend it.

What impressed me most about Ready is the simplicity: flat 3% cashback on Metal, 0% FX fees, no staking requirements. At $333/month in spending, the $120 annual fee pays for itself. One tier list from early 2026 ranked it as the top travel card for crypto users specifically because of the 0% FX plus $800/month free ATM withdrawals.

Community feedback is solid. The app holds 4.5/5 on Apple Store (2,289 ratings) and 4.3/5 on Google Play (7,103 ratings). Users in Asia-Pacific (Hong Kong, Singapore, Japan, Korea) have successfully applied despite the card officially listing UK + EEA only.

Card offers:

- Ready Lite: Free card ($6.99 shipping). 0.5% cashback in STRK. 1% FX fee. $200/month free ATM withdrawals. $30,000 monthly spend limit.

- Ready Metal: 120 USDC/year (no auto-renewal). 3% cashback in STRK on up to $5,000/month (capped at $150/month, $1,800/year). 0% FX fees. $800/month free ATM withdrawals. 10% cashback for first 30 days (up to $1,500 spent).

- Partner perks: Free bridging via Layerswap (up to $100/month), discounted eSIMs (Airalo), Koinly, Nansen, NordVPN

- Google Pay and Apple Pay supported

- USDC-only spending — 1 USDC = 1 USD, no hidden markups

Pros

- Flat 3% cashback on Metal — no staking, no tier complexity

- 0% FX fees on Metal using official Mastercard exchange rates

- True self-custody — funds in your smart contract wallet until spend

- 10% promotional cashback in first 30 days covers the annual fee

- $800/month free ATM withdrawals on Metal

- Strong partner perks (Layerswap, Koinly, Nansen, Airalo, NordVPN)

- Clean app with high user ratings (4.5/5 iOS, 4.3/5 Android)

- No seed phrase required — integrates directly with Ready Mobile

Cons

- 120 USDC annual fee on Metal (Lite is free but only 0.5% cashback)

- Cashback paid in STRK — volatile token, value can fluctuate

- USDC-only spending — must convert other crypto first

- Monthly cashback capped at $150 regardless of spending volume

- Cashback program reviewed quarterly — rates could change

- Not available in the United States

- Gambling, financial transfers, and tax payments excluded from cashback

Best For: Frequent travelers and European crypto users who want a clean, flat cashback structure with zero FX fees and genuine self-custody. The break-even math is simple: spend $333/month and the card pays for itself.

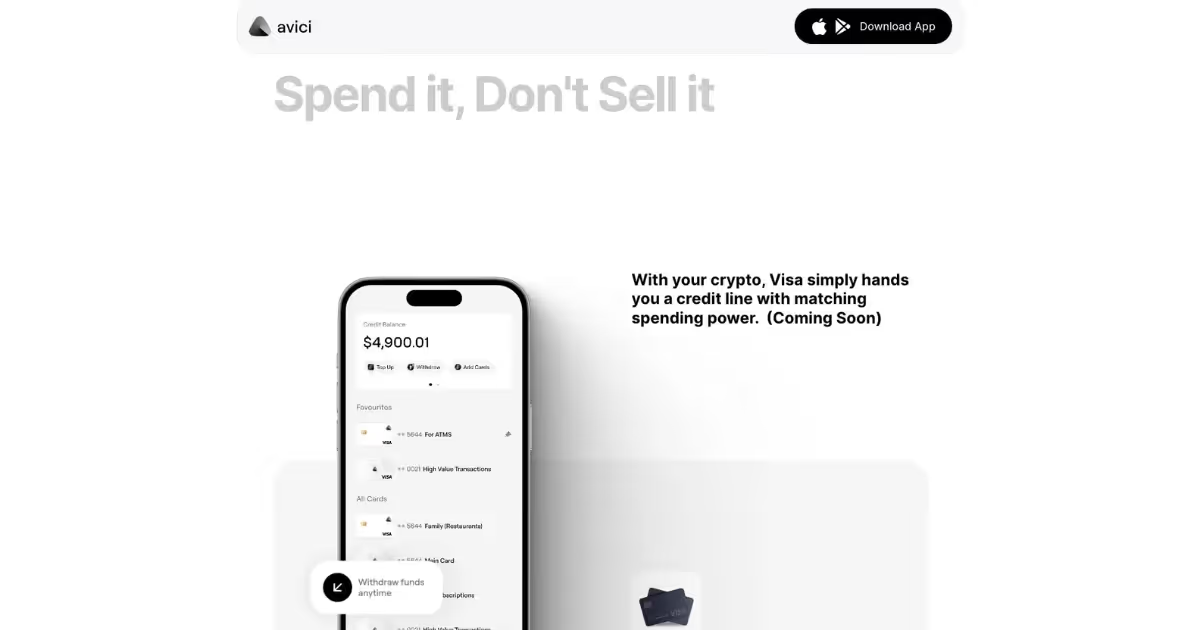

4. Avici

Avici is a Solana-based self-custodial neobank aiming to replace your bank entirely. It's a Visa secured credit card, which means you deposit USDC into a smart contract you control, and that establishes your credit line. No staking, no token lockups, no custodial risk. When Avici shuts down, you keep your unspent collateral. The app uses passkeys and biometrics instead of seed phrases, and sponsors gas fees on Solana and Base so spending feels like a normal bank card.

Virtual cards activate in minutes with Apple/Google Pay. The card claims $0 transaction fees and 0% Avici FX fees — though Visa's cross-border surcharge (0.4–1%) still applies on non-USD merchants. Physical cards ship in 3–4 weeks (or faster with $50 expedited). A Solana maxi, Jussy World shared his seamless experience with Avici in Bangkok, Thailand, where he withdrew USDC into fiat from a random ATM within minutes.

I landed in ThailandFirst thing I needed was cashTook my USDC on @solana, used @AviciMoney. Withdrew from the first ATM I found in 1 minuteDoneUSDC on Solana to cash. That's the future of finance. Source: @jussy_world

Card Offers:

- Self-custodial Visa (Signature/Infinite tiers

- $0 transaction fees, 0% Avici FX fees

- Virtual USD/EUR accounts for fiat on-ramps (Wire/ACH/SEPA)

- Multiple category-based cards for budgeting

- Referral: 20% of referred user's card fee, 10% discount for referee.

- Roadmap: Avici Earn (lending/borrowing), decentralized credit scoring

Pros:

- True self-custody — USDC locked in your own smart contract, not Avici's wallet

- $0 transaction fees and 0% Avici FX fees (Visa cross-border 0.4–1% may apply)

- No staking or token lockups required for any tier

- Passkey/biometric login — no seed phrases

- Gas fees sponsored on Solana and Base

- Virtual USD/EUR accounts for easy fiat on-ramps

Cons:

- No cashback or rewards program — zero spending rewards

- Requires 1:1 USDC collateral for all spending (capital locked up)

- Early-stage — limited track record vs. established cards

- Not available in EU, UK, Canada, China, India, Russia (37 restricted countries)

- Potential liquidation/penalty fees disclosed in terms

- Physical card costs extra; expedited shipping $50

Best for: Self-custody maximalists who want to spend crypto without ever giving up their keys — and don't care about cashback. Strongest for U.S., Latin America, Africa, and Asia-Pacific users locked out of European-focused cards.

5. RedotPay

RedotPay is a Hong Kong-based stablecoin payment platform with over 6 million users across 100+ countries and $10B in annualized payment volume. It's a custodial Visa card that auto-converts USDT/USDC to fiat at point of sale — no pre-conversion needed.

The appeal is simplicity and massive limits: up to $100,000 per transaction, $1,000,000 daily. In February 2026 they launched a dedicated Solana card for spending SOL and Solana-based assets. No monthly or annual fees, but the per-transaction costs add up.

Feedback on Google App is mixed. With users in Asia and Latin America, RedotPay is a lifeline for spending crypto where banking is limited. Some users flag inconsistent NFC/Google Pay behavior and lengthy KYC-related refund delays. From my experience, small BTC transfers under $10 failing to arrive entirely because of the blockchain congestion.

Offers:

- Virtual card: $10 issuance

- Physical card: $100 issuance

- Auto-conversion at POS

- Stablecoin yield on idle balances (mid-single digits)

- Solana card with up to 1.5% cashback promo (limited time)

- Referral program: up to 40% commission on referred users' transactions

- $5 signup bonus with referral

- No monthly or annual fees

Pros:

- Massive spending limits — up to $100K/transaction, $1M/day

- 100+ countries supported, strong in Asia-Pacific and Latin America

- No monthly or annual fees; stablecoin yield on idle balances

- Simple onboarding — KYC under 5 minutes in most cases

- Solana card integration for SOL/SPL token spending

- $10B+ annualized volume — proven at scale

Cons:

- 1% crypto conversion fee on every purchase plus 1.2% FX on non-USD

- No ongoing cashback (promos are temporary and limited)

- Custodial — you transfer stablecoins to their platform

- $100 physical card issuance fee is steep

- Hidden micro-fees: $0.20 per small transaction (after 5th), $0.50 decline fee (after 3rd)

- Not available in the U.S., parts of Europe, Ukraine, Russia

Best for: High-volume spenders and users in banking-limited regions (Asia, Latin America) who need massive daily limits and don't prioritize cashback. Less ideal for everyday low-spend users where the 1%+ fees erode value.

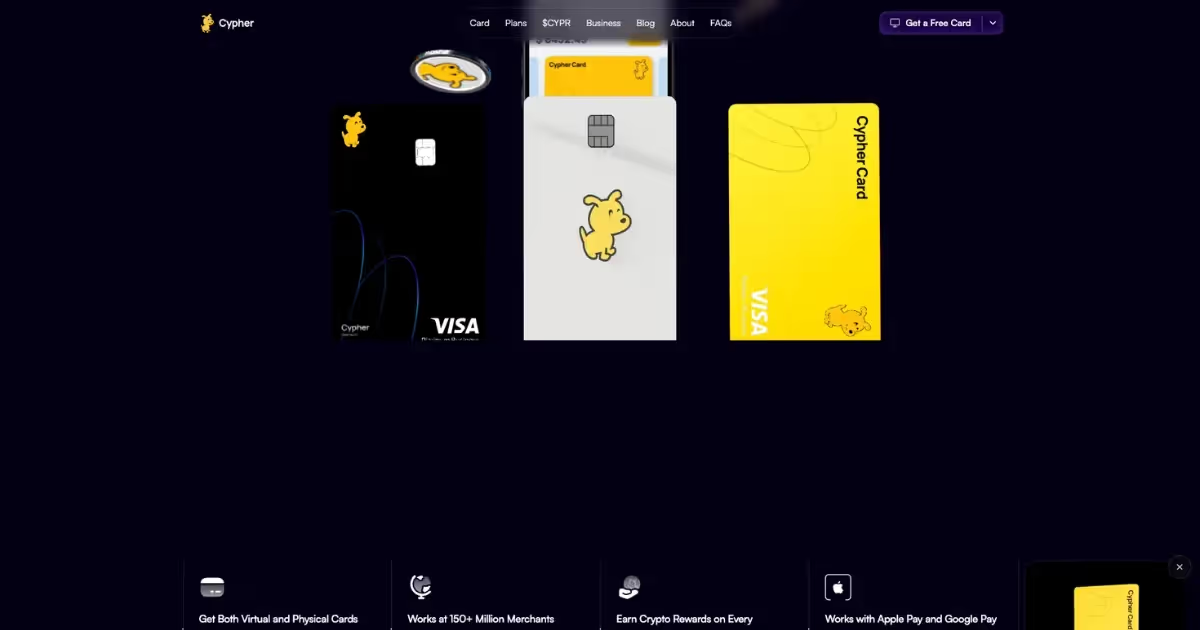

6. Cypher

Cypher (formerly CypherD) is a Y Combinator-backed Web3 financial platform that combines a non-custodial, multi-chain wallet with a Visa spending card. It supports 500+ tokens across 25+ blockchains — from Ethereum and Solana to Base and Cosmos — making it one of the broadest multi-chain crypto cards available. The card converts crypto to fiat in real time at the point of purchase.

Cypher's Visa card generated $20.5M in net spend in 2025, ranking second among major crypto cards.

Community feedback on X is enthusiastic. Even Base's Ecosystem Lead David Tso acknowledged Cypher with a public shoutout on X for its composability with Base and Coinbase assets.

You can now use major cbAssets on @base like cbBTC, cbETH, cbXRP, cbDOGE, cbADA, and cbLTC for everyday spending with your @Cypher_HQ_ card. Source: David Tso

Cypher is also building business tools — KYB onboarding, multi-card issuance, accountant access, and integration with Gnosis Safe for treasury management.

Card offers:

- Standard (Free): Virtual card instant after KYC. Physical plastic card (shipping fee). 0.5% USDC load fee, 1% other tokens. 1.75% FX markup. 3% ATM fee. $4,000 daily spend limit.

- Premium ($199/year): Metal card with free shipping. 0% USDC load fee, 0.5% other tokens. 0.75% FX markup. 2% ATM fee. Up to $300 fraud protection.

- Up to 5% cashback in CYPR tokens on eligible spending (boosted merchant campaigns)

- CYPR rewards ecosystem — lock into veCYPR for boosted rewards and governance

- Apple Pay and Google Pay supported

- Business accounts with multi-card issuance and accountant access

Pros

- Supports 500+ tokens across 25+ blockchains — broadest multi-chain support

- Non-custodial wallet — crypto stays in your control until conversion

- Global availability including 33 U.S. states

- Y Combinator-backed with proven spending volume ($20.5M in 2025)

- Business/team spending tools with KYB support

- Strong community feedback and responsive customer support

- Boosted merchant rewards with user-voted CYPR incentives

Cons

- Standard tier has 1.75% FX markup and 3% ATM fees

- Premium costs $199/year — only worthwhile for frequent spenders

- Cashback in CYPR tokens is variable, not flat — depends on campaigns

- $4,000 daily spend limit (Standard) is lower than many competitors

- Must pre-convert crypto to USD before spending

- No free ATM withdrawals on any tier

Best For: Multi-chain DeFi users who hold assets across many networks and want a single spending card without constantly bridging. Also strong for crypto businesses needing expense management tools.

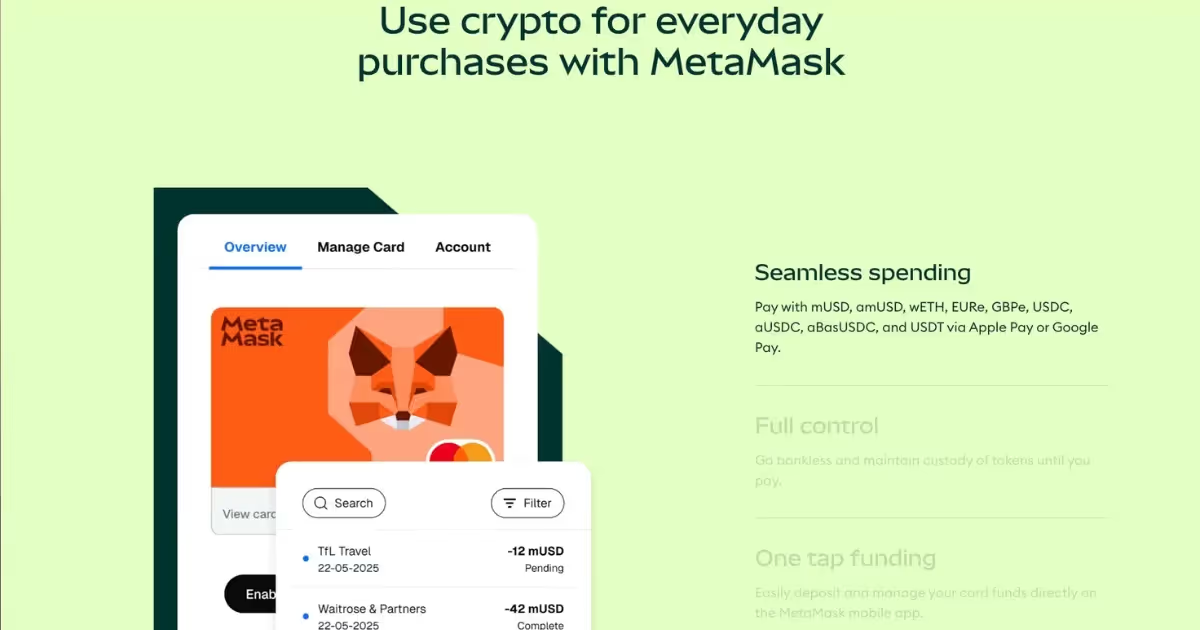

7. MetaMask Card

The MetaMask Card connects directly to your MetaMask wallet on Linea (Ethereum L2), letting you spend crypto from your own address while maintaining key custody until the moment of payment. It runs on Mastercard and supports USDC, USDT, wETH, EURe, GBPe, and aUSDC — though U.S. users are limited to USDC and aUSDC only.

When it works, the integration with MetaMask's existing app is seamless. The Linea L2 infrastructure keeps gas costs low, and Linea Boosted Yield on Aave is a nice bonus for idle funds. But the pilot-phase limitations make it feel like a product still finding its footing.

Card Offers

- Virtual Card: Free. 1% crypto cashback in USDC on all eligible transactions. $10,000 per transaction, $15,000/day limit.

- Metal Card: Premium physical metal card. 3% cashback on first $10,000 spent yearly (1% thereafter). $20,000 per transaction, $30,000/day limit. Higher ATM limits and exclusive perks.

- Free ATM withdrawals up to $1,200/month (2% above)

- Apple Pay and Google Pay supported

- Linea Boosted Yield on Aave and Linea Coinmunity Cashback perks

Pros

- Six supported tokens — USDC, USDT, wETH, EURe, GBPe, aUSDC

- 3% cashback on Metal for first $10K/year — competitive for moderate spenders

- Free ATM withdrawals up to $1,200/month

- Clean integration with MetaMask app and Linea L2

- Apple Pay and Google Pay supported

- Linea ecosystem perks (Boosted Yield on Aave)

Cons

- Still in pilot phase — limited regional access with waitlists

- U.S. early access ended; waitlist for next launch

- Cashback details unclear and not consistently applied

- Requires managing Linea wallets, gas fees, and token conversions

- Available in select countries only (Europe, UK, Argentina, Brazil, Colombia, Mexico — excluding some EU states)

- Fewer fiat conveniences compared to neobank-style cards

Best For: Existing MetaMask users in supported regions who want a native spending extension for their wallet without switching ecosystems.

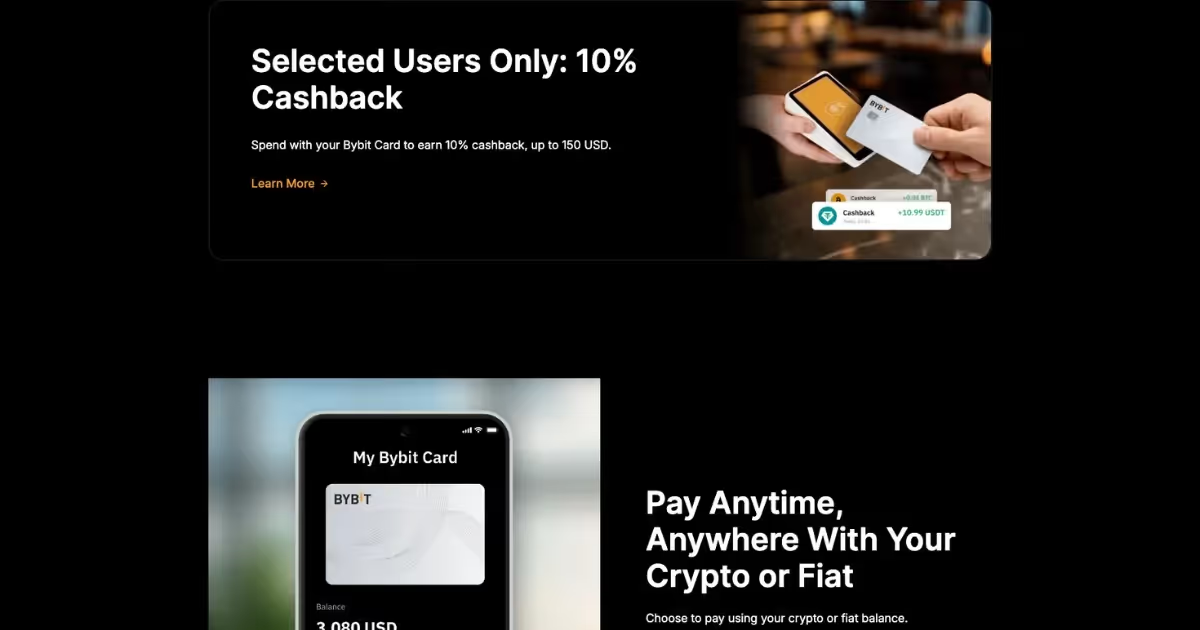

8. Bybit Card

Bybit Debit Card is purpose-built for users already living in Bybit. It lets you spend crypto directly via Mastercard, earns tiered cashback, and links seamlessly with Bybit Pay. The latest update merges both services into one reward system, meaning every transaction helps you climb tiers and unlock higher rewards. The Auto-Savings function is underrated — it automatically earns interest on assets in Flexible Savings, which you can unstake and spend at any time.

Card Offers:

- Up to 10% cashback for high-tier users (limited-time promos reach 20%)

- 10% rebates on selected partners: Netflix, ChatGPT, Spotify, Amazon Prime, TradingView

- Auto-Savings function — earn interest on Flexible Savings, unstake and spend anytime

- $100 USD in free ATM withdrawals monthly

- Apple Pay, Google Pay, and Samsung Pay compatible

- No annual fee in most regions

- Integrated with Bybit Pay for unified rewards and faster tier progression

- Competitive FX rates (~0.5–1%)

Pros

- Up to 10% cashback for top-tier users with subscription rebates

- Auto-Savings earns yield on idle balances automatically

- $100/month free ATM withdrawals

- Triple mobile wallet support (Apple Pay, Google Pay, Samsung Pay)

- No annual fee; competitive FX rates

- Unified rewards with Bybit Pay accelerate tier progression

Cons

- Base cashback is low — high rates require significant Bybit trading activity

- 0.9% crypto conversion fee stacks on top of spot fees

- Most high-rate campaigns are temporary or region-specific

- Only available in Australia and EEA countries

- Cashback tiers are complex and conditional

Best For: Active Bybit traders in Europe or Australia who want their trading activity to translate into everyday spending rewards. Less compelling as a standalone card.

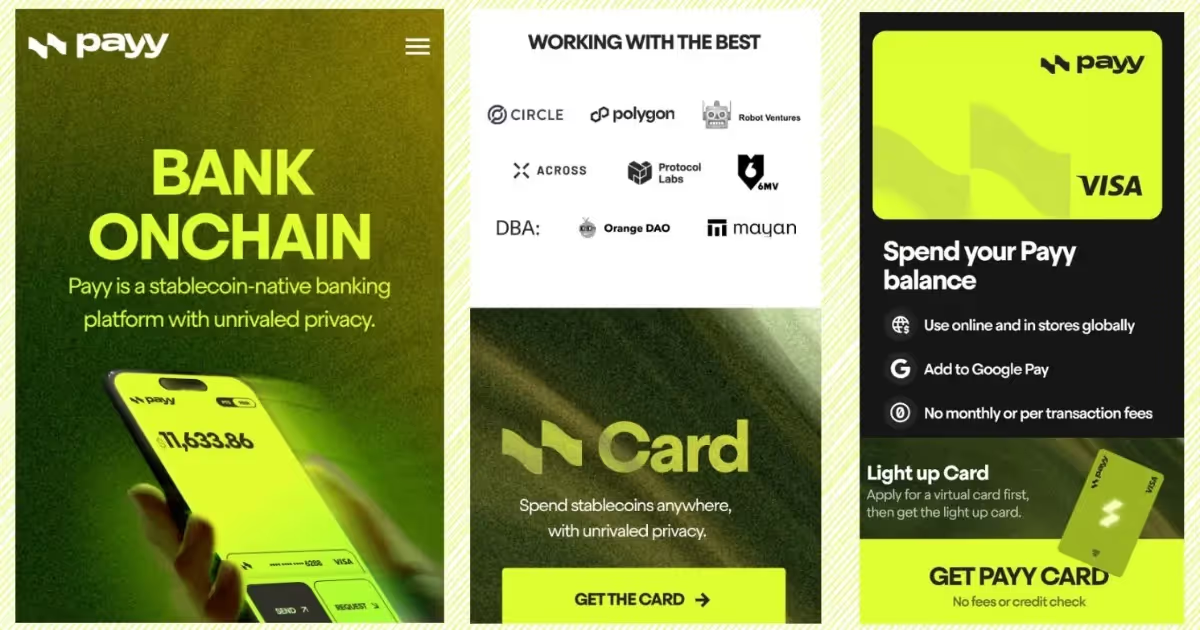

9. Payy Card

Payy is a newer crypto card and wallet combo designed around privacy and stablecoin spending. It offers a self-custodial Visa card that lets you spend USDC via its own zk-enabled "Payy Network," aiming to hide on-chain linkages between your identity, wallet, and card purchases. The physical card even lights up when you tap it — a unique touch that differentiates it from the sea of generic crypto cards.

Card Offers

- Self-custodial Visa card with USDC spending

- Zero-knowledge privacy layer — transactions and wallet balances not publicly traceable

- Light-up physical card design

- No transaction or top-up fees (per documentation)

- Points/rewards program in development

- Fiat ramps being expanded

Pros

- Privacy-first design — zk-enabled system hides wallet-to-card linkages

- Non-custodial — you keep control of funds in Payy Wallet

- No transaction or top-up fees reported

- Unique physical card design (light-up on tap)

- Clean approach to stablecoin spending

Cons

- Rewards/cashback minimal or not clearly defined yet

- Still early stage — fiat ramping and global availability under rollout

- Doesn't compete feature-for-feature with full neobanks (no yield, no lending)

- Regulatory/licensing risk as a non-traditional card

- Limited community feedback so far — hard to verify daily experience

Best For: Privacy-conscious crypto users who value zero-knowledge transaction obfuscation over cashback rewards. Best suited for early adopters willing to trade maturity for privacy.

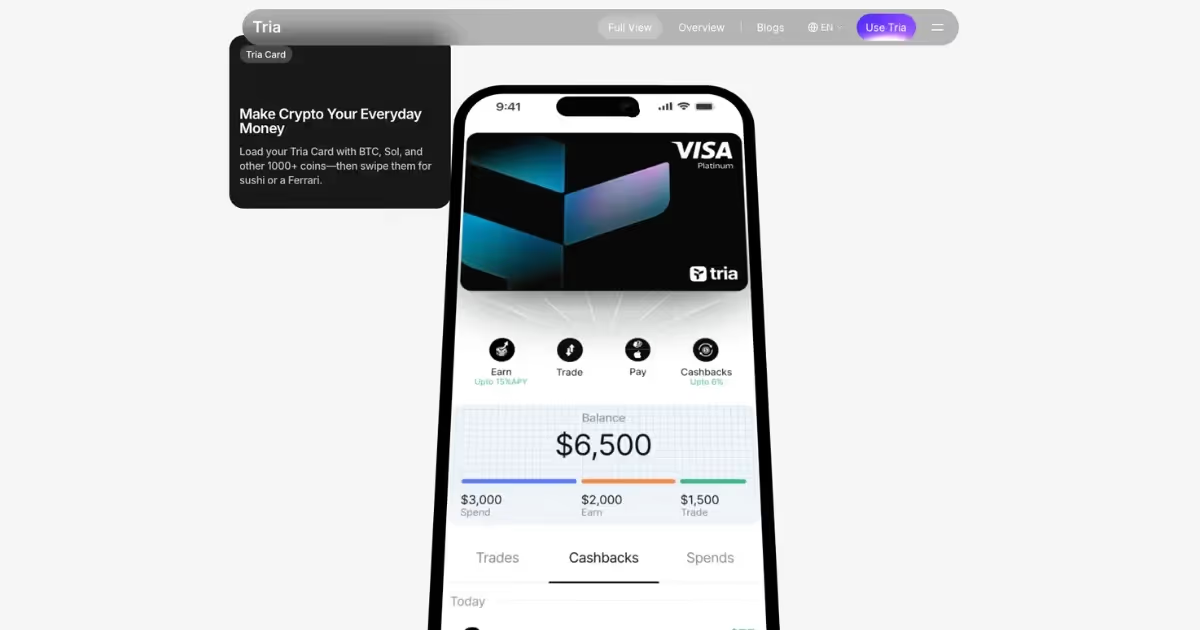

10. Tria

Tria positions itself as a "borderless Web3 neobank" — aiming to make crypto spending feel as smooth as a modern banking app. You can top up with over 1,000 tokens, trade and earn directly in the app, and use the card in more than 150 countries.

Powered by its BestPath engine, Tria automatically handles gas and cross-chain routing, so you don't need to worry about bridges or paying gas in different tokens.

Tria raised $12M in late 2025 to scale its global rollout, and it's starting to look like one of the stronger self-custodial neobank contenders for users who don't want to think about which chain their money is on.

Card Offers

- Up to 6% cashback for active users

- 1,000+ supported crypto assets

- No interest on purchases; simple onboarding

- Gasless, cross-chain UX powered by BestPath engine

- Works in 150+ countries

- Airdrop potential for early users

- Virtual and physical card options

Pros

- Works globally with support for 1,000+ crypto assets

- Up to 6% cashback for active users

- Gasless, cross-chain UX eliminates bridging headaches

- Simple onboarding and clean app design

- $12M funding gives runway for global expansion

- Airdrop potential for early adopters

Cons

- Up to 3% FX fee on non-USD transactions

- Cashback tiers and promos can change over time

- Some features (multi-chain credit, advanced rewards) still rolling out

- Card delivery and customer support vary by region

- Newer product — less community feedback compared to established cards

Best For: Users who hold assets across many chains and want a single neobank-style app that abstracts away gas and bridging complexity. Strong option for global travelers.

Comparison Table: Top 10 Crypto Cards at a Glance

What to Watch Next

The crypto card space is heading toward a convergence point. DeFi lending protocols are directly integrating with card issuers, which means the line between your Aave position and your grocery spending is about to blur even further. MiCA regulations in Europe are reshaping how these products operate in the EEA, and DAC8 reporting requirements will change how cashback and rewards are taxed across the EU.

For now, my wallet has two slots filled with EtherFi and Ready. If you're considering jumping in, start with whatever ecosystem you're already using, the switching costs between crypto cards are higher than you think, and KYC fatigue is real.

FAQ

Which crypto card has the best real cashback rate in 2026?

It depends on your spending currency and location. Ready Metal (3% STRK, 0% FX) for predictability. Cypher for multi-chain users chasing boosted merchant rewards. Gnosis Pay's 4–5% in GNO looks great until the token drops 15% in a week. RedotPay and Avici offer no ongoing cashback.

Are crypto cards safe to use for everyday spending?

Self-custodial cards like Gnosis Pay, Ready, Avici, and Ether.fi keep your funds in your own wallet until the point of sale, which is a significant security upgrade over exchange-linked cards. However, none of these carry FDIC insurance or traditional bank protections. Treat them as spending tools, not savings accounts.

Do I have to pay taxes on crypto card purchases?

In most jurisdictions, yes. Every time you spend crypto through a card, you're technically disposing of an asset, which can trigger capital gains tax. This applies even to stablecoins in some regions. Consult a tax professional — this is not financial advice.

What's the biggest hidden cost with crypto cards?

Foreign exchange fees and conversion spreads. Most cards advertise zero or low transaction fees, but the FX markup on non-native currency purchases can range from 1–3%. Always check whether the fee structure changes for cross-border transactions. Ready Metal and Bleap stand out for genuinely offering 0% FX.

Can I use crypto cards outside of Europe?

Yes, but availability varies widely. Cypher covers 33 U.S. states plus global markets. RedotPay works in 100+ countries (strong in Asia and Latin America, no U.S.). Avici covers U.S., Latin America, Africa, and Asia-Pacific. Tria claims 150+ countries. MetaMask covers Europe, UK, and select Latin American markets. Gnosis Pay, Ready, and Bybit are primarily EEA/UK. Payy is still rolling out. Always verify your country on the issuer's site before applying — regional restrictions change frequently.

Which crypto card is best for beginners?

RedotPay if you're outside Europe and just need simple stablecoin spending with high limits. Bybit if you're already on the exchange. Anything requiring Safe wallets, collateral monitoring, or multi-chain bridging adds friction beginners don't need.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Crypto investments carry significant risk including potential loss of capital. Always do your own research before making financial decisions. Data sourced from DefiLlama, Dune Analytics, The Block, CoinGecko, Trustpilot, and direct product testing. Cashback rates, fees, and features are subject to change — verify current terms on each provider's website before applying.

.png)

%201.svg)

%201%201.png)