The RWA Tokenization Playbook 2026: A Beginner Guide

9 mins

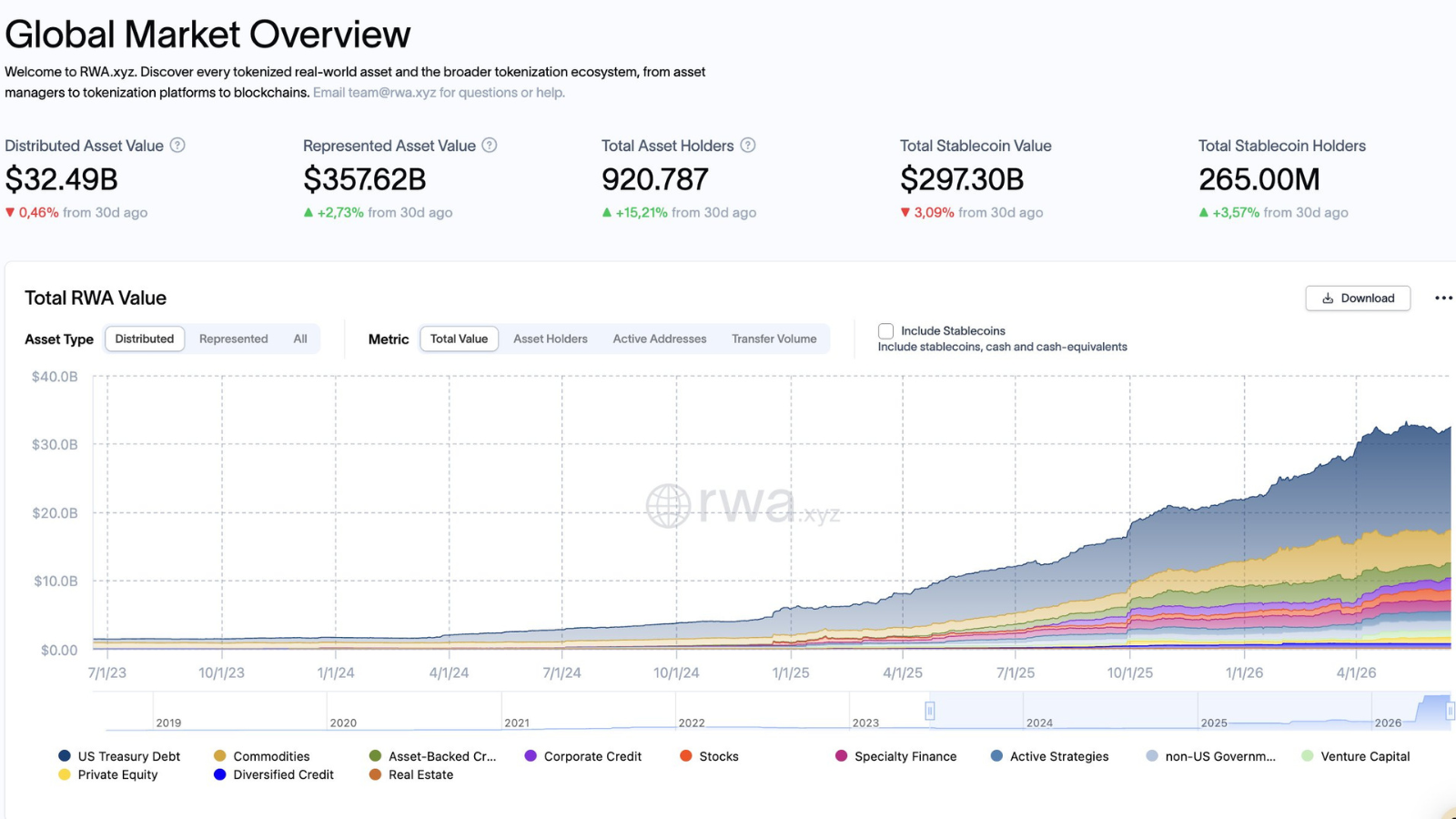

Standard Chartered predicts tokenization could push real-world assets (RWAs) onchain to $2.7 trillion by 2030. Today's global tokenized RWA market cap has nearly quadrupled in 15 months, from $5.42B at the start of 2025 to $32.49B now.

However, the "RWA" most normies trade is rarely the asset.

When someone says they're "in RWAs," they usually mean buying a protocol's governance token. 6 of the 7 top RWA project tokens posted negative returns of -30% to -50% since the start of 2025, even as the underlying sector skyrockets. The rest of the top RWA players either will never launch a token or are still pre-TGE. Meanwhile, the S&P 500 keeps hitting new highs as investors pile into AI, chipmakers, and tech stocks, betting that the AI boom is still in its early innings.

The upside is in the assets. Narrative tokens are the beta play (until fees or revenue start flowing back to tokens). That's why the optimal strategy for normies is getting exposure to the assets and layers.

This RWA tokenization playbook is a place to start.

Which real-world assets are tokenized?

We’ll look at the 4 most common tokenized asset classes: government debt, credit funds, tokenized equities, and commodities.

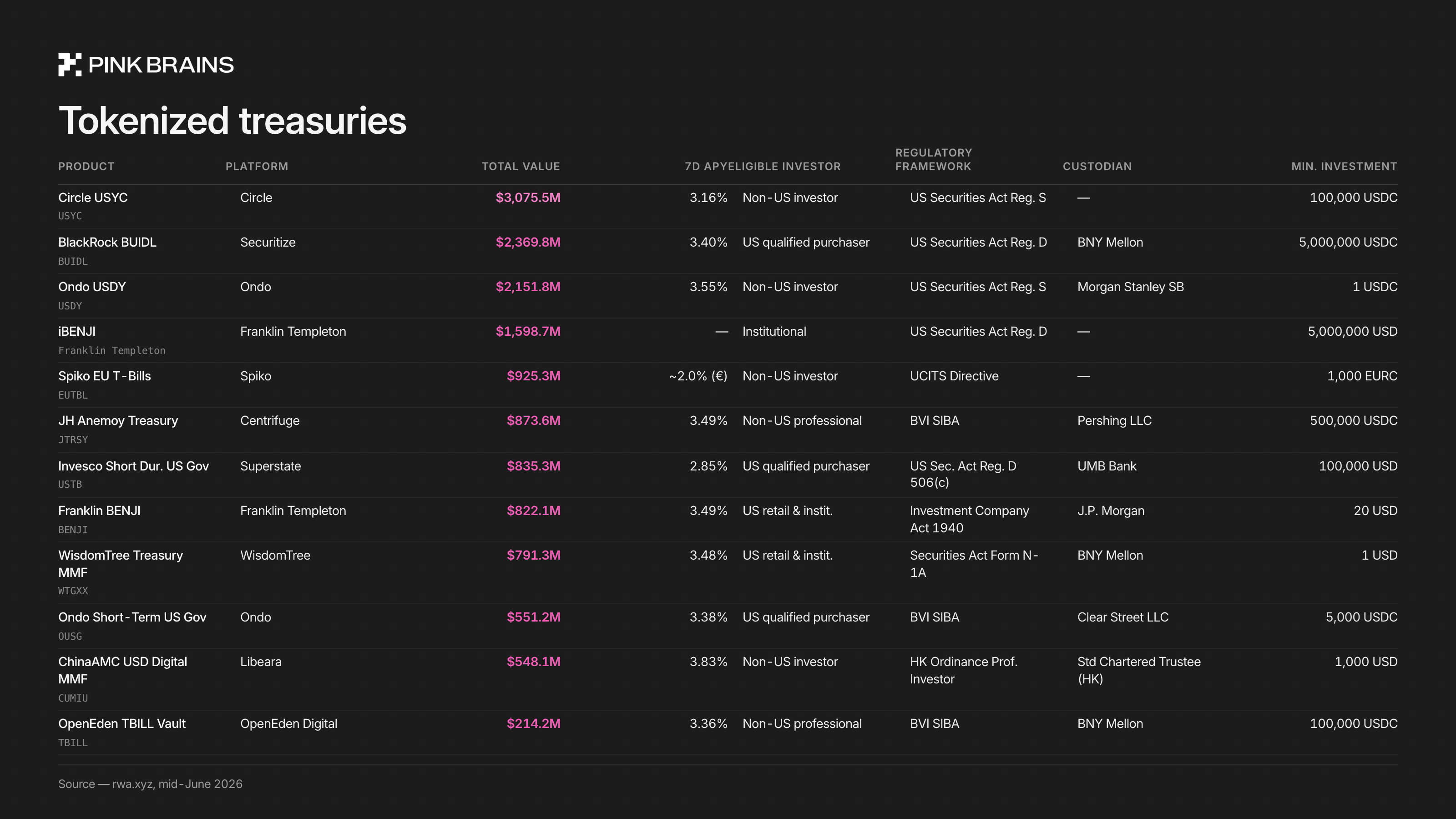

1. Government debt (US and non-US treasuries)

Treasuries are one of the easiest RWAs to bring onchain because they're simple, trusted, and generate a predictable yield backed by governments, usually US Treasury bills, and increasingly Euro bills.

When you hold the token, your money is effectively invested in those bonds, so you earn the same yield they generate.

When interest rates were around 5%, many investors moved into tokenized treasuries to earn that yield onchain. As a result, the market grew from $4B at the start of 2025 to over $16B by June 2026.

The yield is nearly identical everywhere (~3-4%) because they all hold the same T-bills. Choose which to buy depending on your capital and where you're based. For example:

- BENJI lets US retail in for $20

- USDY lets non-US retail in for 1 USDC

- BUIDL and iBENJI gate at $5,000,000 for institutions only

If you don't want exposure to U.S. T-bills, Spiko EU T-Bills Money Market Fund deserves a callout as the main euro option: $925.3M total value, open to non-US investors, 1,000 EURC minimum. It's a short-term money-market fund under EU law, holding 100% Eurozone investment-grade government T-bills, repos secured by them, and cash (capped at 10%). It keeps average portfolio maturity under 60 days and max maturity under 6 months.

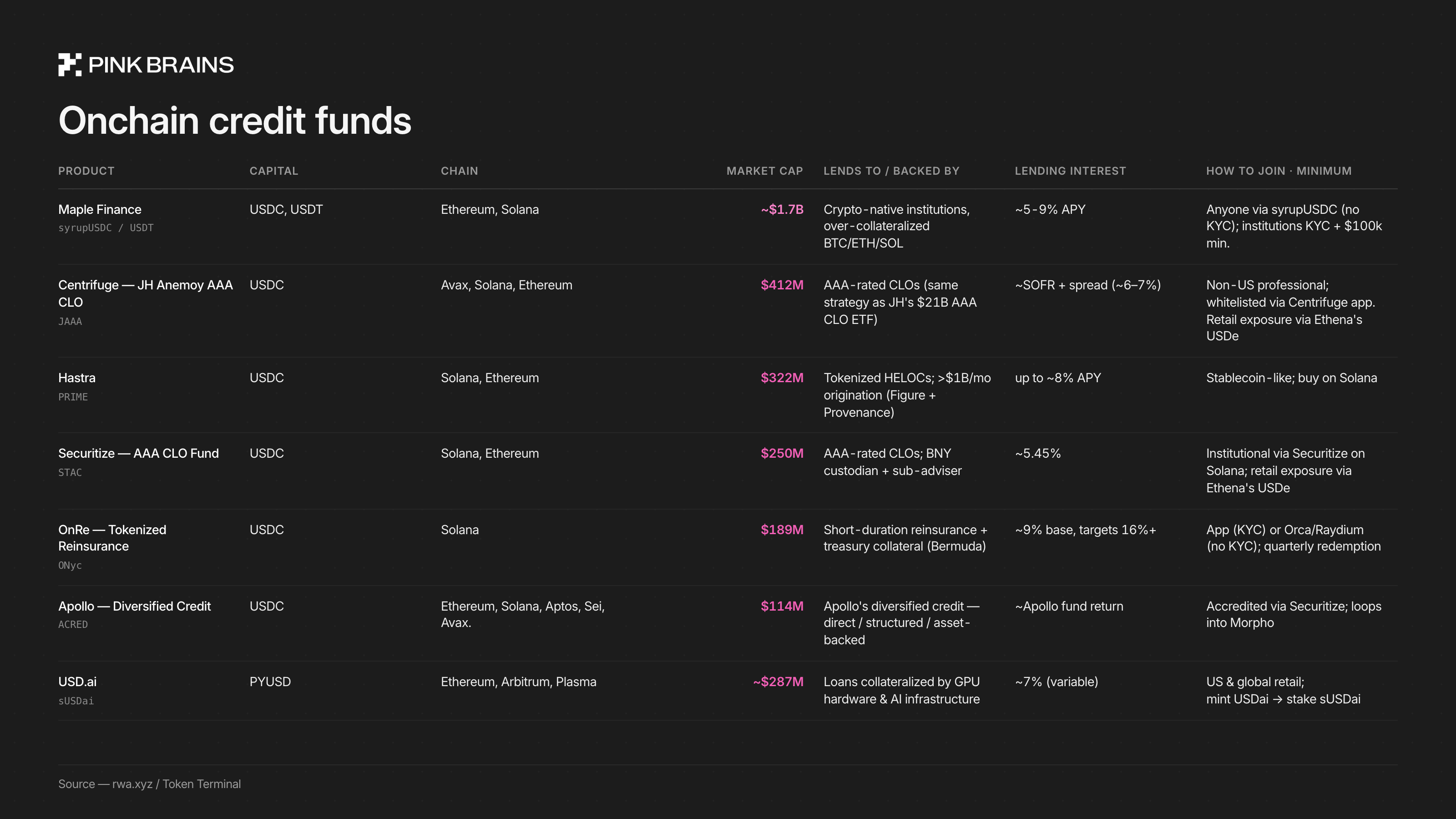

2. Credit funds

Private credit is when you lend money directly to businesses instead of buying government bonds or public company debt. But in fact, you don't lend it directly to business owners. Your money is pooled into a lending platform, which then makes loans to companies, funds, or traders. In return, investors earn higher yields.

You earn more than T-bills (often 8-12% or more) precisely because you're taking real risk. The category has broadened well beyond plain lending into AAA-rated CLOs, AI-hardware financing, and even reinsurance.

Onchain private credit grew from $400M at the start of 2025 to $6.1B in June. Here are the 7 biggest products, with what each takes in, who it lends to, the rate, and how you join.

- Maple Finance's lead reflects crypto trading-desk borrowing, not real-world lending. Other assets are growing fast in market share.

- JAAA and STAC bring institutional AAA CLOs onchain (and into Ethena's USDe backing)

- PRIME tokenizes real mortgage credit

- USDai finances the AI hardware boom

- ONyc (OnRe) opens reinsurance - an asset class normally walled off from retail

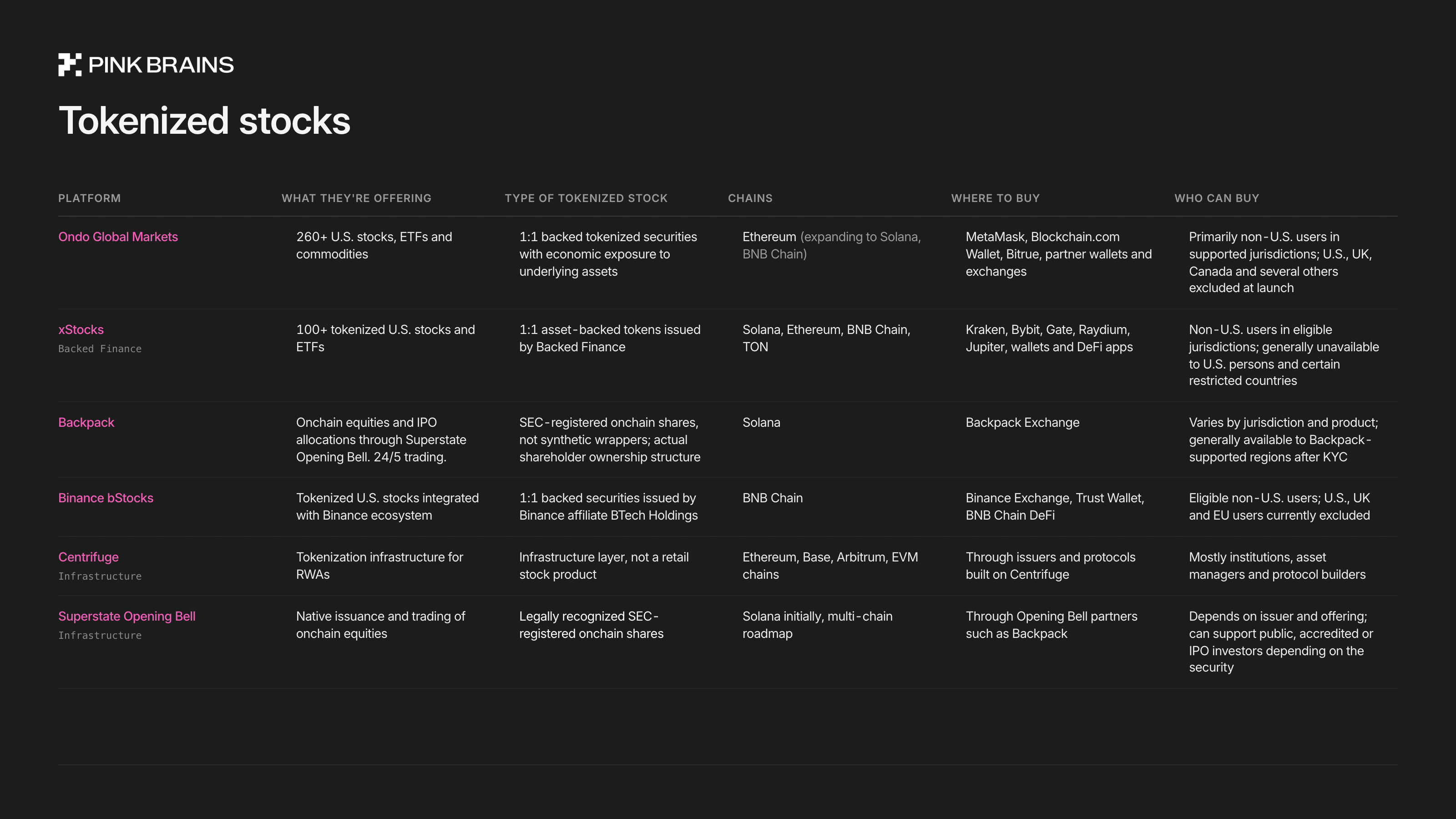

3. Tokenized equities

Public Equities

There are 2 main types of tokenized stocks.

Type 1: Wrappers

The issuer buys the real share, locks it with a custodian, and sells you a token that mirrors the price. You get the price exposure and DeFi composability, but no shareholder voting rights, and the peg holds only as long as the issuer's redemption works.

Most tokenized stocks today are sold under Reg S-style frameworks, meaning they're generally available to non-U.S. investors after KYC while excluding U.S. retail users. xStocks, Ondo, and bStocks largely follow this model. This is most of the market today.

Type 2: Real 1:1 tokenized stocks

Here the token is legally tied to a real share, which means you can redeem it for real stocks with dividends and corporate actions through rebasing.

Superstate Opening Bell is different because it is trying to make the share itself natively onchain. Eligibility can therefore vary by issuer and offering, potentially allowing broader participation if the underlying security is registered appropriately. This is closer to the future vision of "Nasdaq onchain".

For crypto investors:

- Ondo → winning on TVL and breadth of assets.

- xStocks → winning on distribution and ecosystem integrations (airdrop potential)

- bStocks → Binance's integrated ecosystem play

- Backpack → most ambitious attempt at bringing actual equity issuance onchain, growing in spot volume

Private equities

These let you bet on companies that haven't gone public yet, such as OpenAI, Anthropic, Kalshi, or Polymarket.

Notably, several private companies went public in June. Quantinuum listed on Nasdaq on June 4. SpaceX followed on June 12, trading under the ticker SPCX. OpenAI filed a confidential S-1 with the SEC. That's why this sector is going to boom bigger in the next few months.

There are 2 ways you can be exposed:

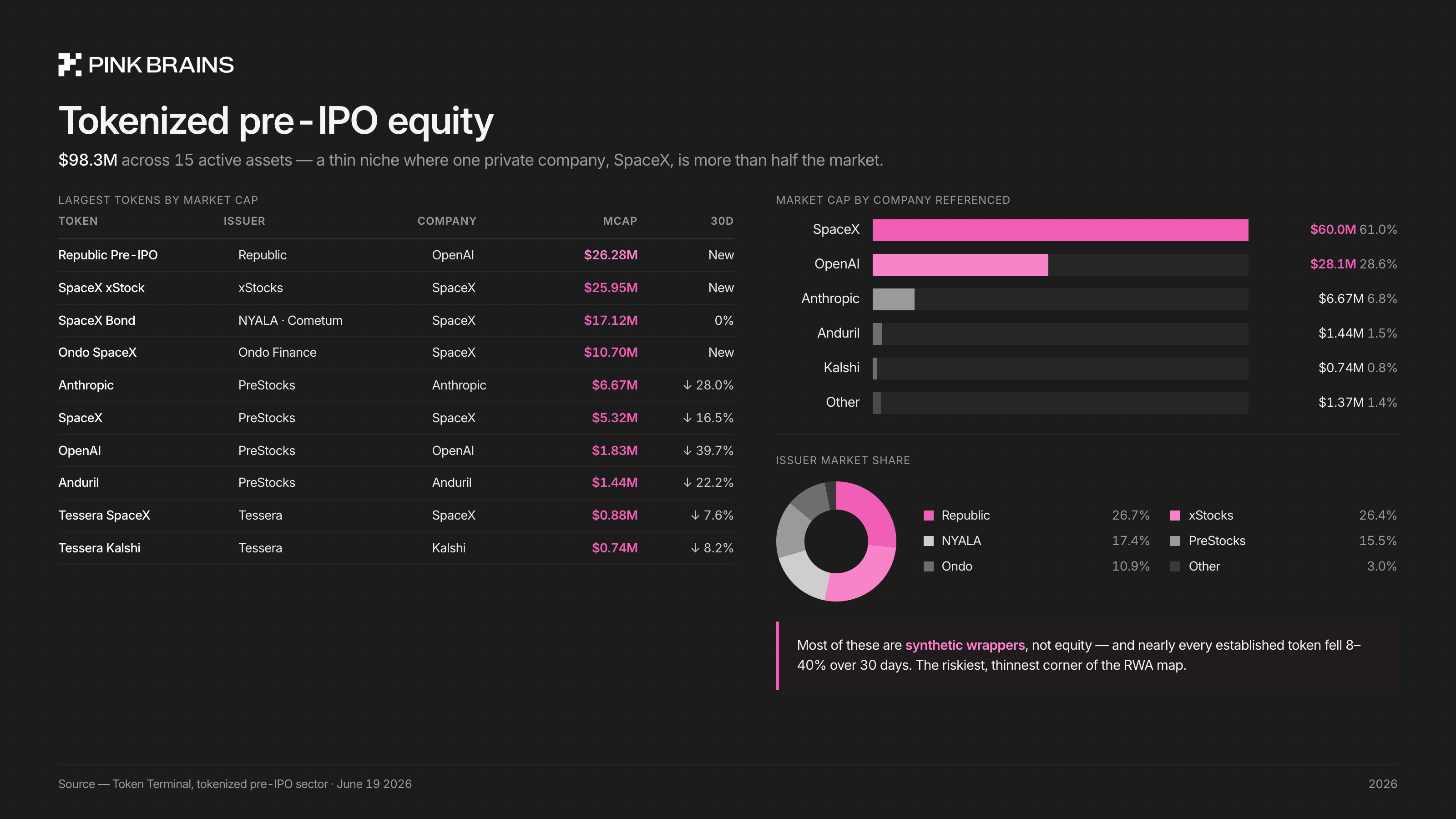

- Tokenized pre-IPO equity: gives you exposure to real private company shares held by an issuer or SPV. The market is still relatively small at around $98M, with most activity centered around SpaceX and OpenAI. Some issuers: Republic, PreStocks, YALA Digital Asset AG, Tessera.

- Pre-IPO perpetuals: bets on price. Volume in these products climbed from $2M in March to $12B in June. Although CEXs like Binance and Bitget now hold 80% share of all pre-IPO perpetual trading, perp DEXs are more fun with potential airdrops (Variational, TradeXYZ through HIP-3).

Things to know before getting into:

- Neither gives you equity. Spot tokens are a claim on an SPV; perps are price bets with no shares, votes, or dividends.

- SpaceX IPO'd June 12 at $135 (~$1.75T, biggest ever). The perps called it early but ran ~15-30% hot. Perps don't become stock. They rebase or convert to a normal perp.

- Ventuals (a top pre-IPO perp project on Hyperliquid) is shutting down its pre-IPO markets. An earlier oracle glitch crashed its SpaceX contract ~45%. Oracle reliability is the real risk, since there's no live spot price to anchor to.

Tokenized ETFs

Most tokenized ETFs are the same wrapper idea as tokenized stocks, but the underlying is a fund (S&P 500, a silver trust, a bond ETF).

ETFs are now ~26% of the category. The two biggest providers are Ondo, xStocks, and 8 of the 10 largest tokenized ETFs are Ondo-built. Top 5 by market cap:

- IVVon ($67.6M): Ondo iShares Core S&P 500

- SPYx ($42M): Ondo State Street SPDR S&P 500 ETF Trust

- IBITon ($41M): Ondo iShares Bitcoin Trust

- QQQon ($38.4M): Ondo Invesco QQQ Trust

- SPYon ($41.8M): xStock State Street SPDR S&P 500 ETF Trust

The S&P 500 has grown this year mainly because investors expect big U.S. companies to keep making more money, especially from the AI boom. Strong company earnings, continued spending on AI infrastructure, and hopes for lower interest rates have helped push stock prices higher. Not interested in US ETFs, or looking for more ETFs beyond the S&P 500? Backpack offers ETFs from emerging markets like Korea, Japan, China, the UK, India, and more, as well as ETFs of Gold, Silver, Biotech, Semiconductor...

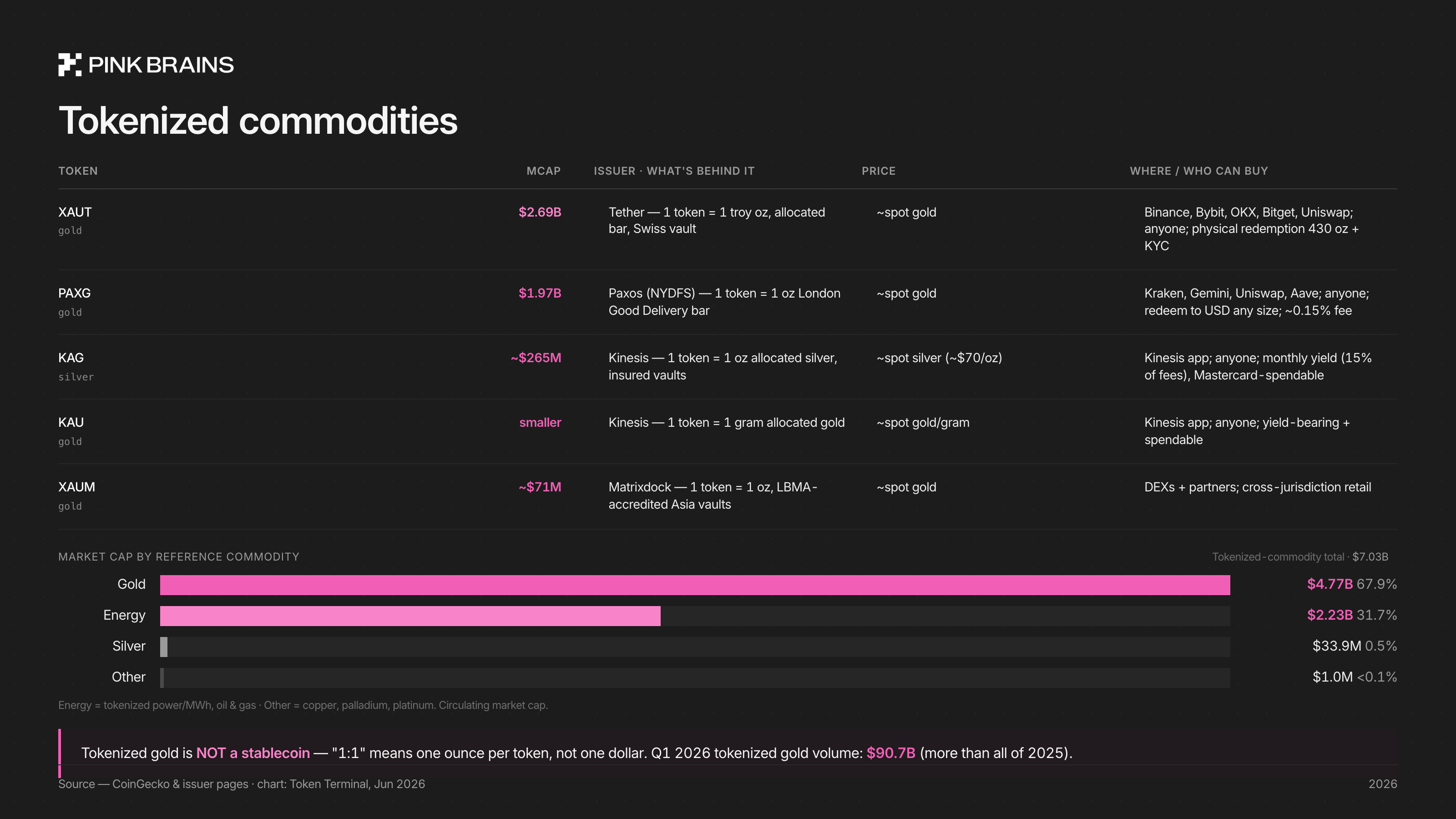

4. Commodities

Commodities reached $5.55B, and gold is ~90% of it.

Instead of buying gold bars, you buy tokens backed 1:1 by real physical gold stored in secure vaults. You can hold them in a crypto wallet, trade them 24/7, and use them in DeFi while still getting exposure to the price of gold.

The market is dominated by XAUt (Tether) and PAXG (Paxos). Other notable projects include Matrixdock Gold, Kinesis Gold, and Comtech Gold, though they're much smaller than PAXG and XAUT.

Where to buy: PAXG and XAUT are both available on most CEXs and major DEXs like Uniswap and Pancake, or through DEX aggregators (Jumper, Kyber, 1inch, Bungee) for the best quotes. PAXG is generally viewed as the more regulated option, while XAUT has deeper liquidity and a larger market size.

One thing to keep in mind: unlike holding physical gold yourself, you are relying on the issuer, custodian, KYC, and your local regulations to safeguard and redeem the real gold. That's the main tradeoff to buying physical gold.

However, tokenized gold can be more capital efficient than physical gold. You can use assets like PAXG or XAUt as collateral in DeFi lending markets to borrow stablecoins (though adoption is still relatively small), or earn yield on gold through yield-bearing tokenized gold products like Theo Network's thGOLD (still on waitlist).

Notably, tokenized energy is starting to appear on the leaderboard as well. Justoken's JMWH, representing real-world electricity measured in MWh, has grown to over $2.2B in tokenized value on Ripple's XRP Ledger. However, it's not available to retail investors yet and is mainly held by a small number of institutions.

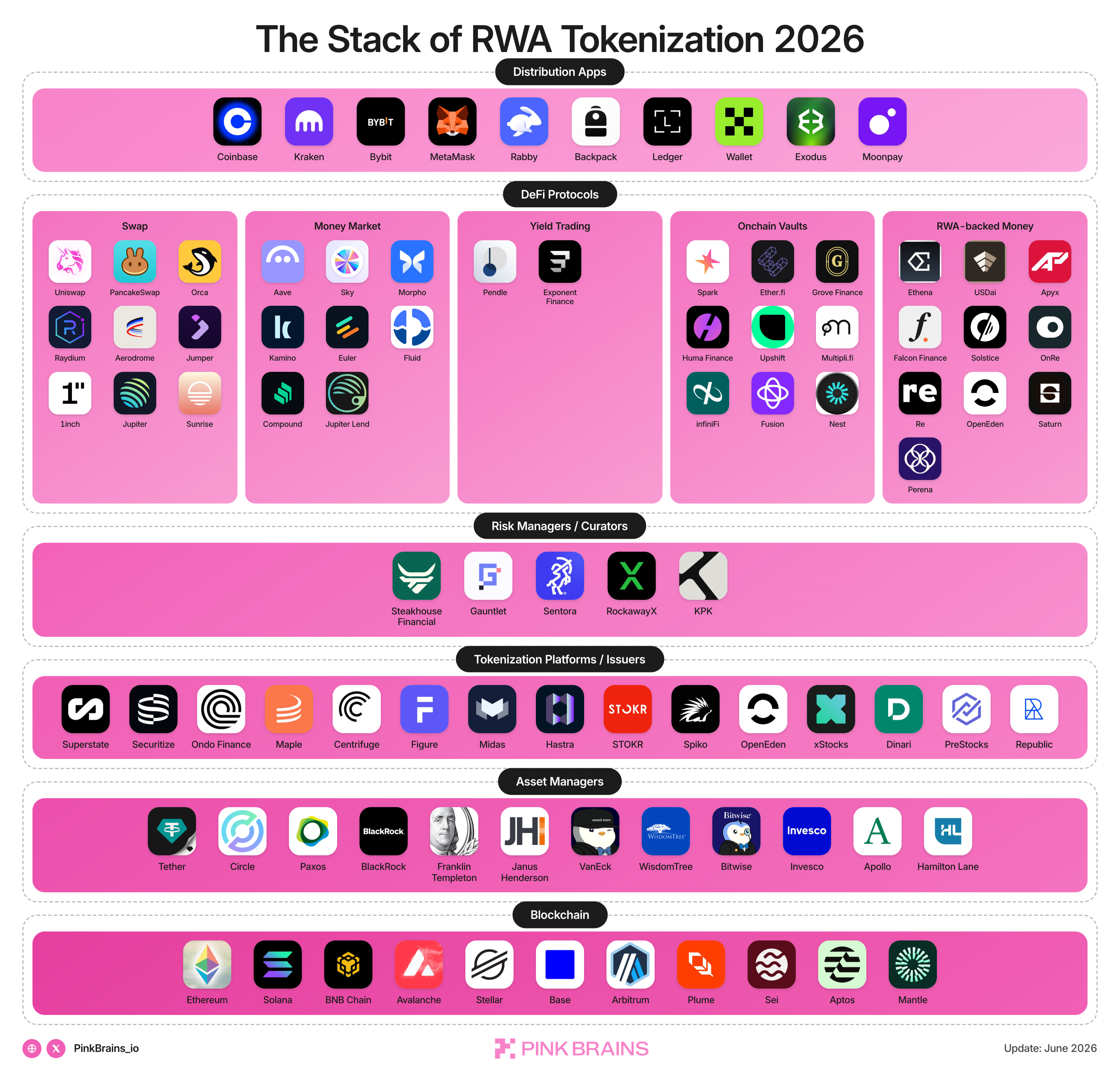

The Stack of RWA Tokenization 2026

By now, you've probably come across a lot of names. To make things easier, here's a quick guide to the key players and where they're in the stack.

L0: Blockchains

The RWA landscape is becoming much more multi-chain.

Ethereum is still where most of the RWA value sits, with $16.2B in distributed RWAs. That's where major issuers like BlackRock and Franklin Templeton launched their products, so institutional capital gravitates there.

But growth is happening elsewhere.

- BNB Chain has grown to nearly $4B in RWAs, being the main chain for USD1, and the growing bStocks.

- Solana has become the most active ecosystem with +2,100 assets and almost 289k holders, largely driven by xStocks and Backpack tokenized stocks.

- Stellar leads all chains in 30-day net inflows (+$525M), fueled by growing demand for Spiko's tokenized EU T-bills.

Not all RWA value is created equal. On Ethereum, BNB Chain, Solana, and Stellar, most assets are issued and settled onchain, which means users can trade and hold them. On other chains like zkSync and XRP Ledger, a large share of the value comes from assets that originate offchain, blockchain only serves as a record-keeping layer for better transparency.

L1: Asset Managers

Asset managers represent the foundational layer of the RWA tokenization stack. These entities are the legal and financial institutions that originate, hold, and actively manage the underlying traditional assets - such as U.S. Treasury securities, money market funds, equities, private credit portfolios, and precious metals - before or during their tokenization.

Their primary responsibility is not merely issuance, but the ongoing stewardship of capital: they ensure asset custody, regulatory compliance, fund administration, and redemption guarantees. In most structures, they operate within established financial frameworks and are subject to jurisdiction-specific oversight, which is a key factor in maintaining investor trust and institutional adoption.

Examples include major global asset managers and financial institutions such as Tether, Circle, Paxos, BlackRock, Franklin Templeton, Janus Henderson, WisdomTree, Bitwise, Invesco, and VanEck.

In the context of tokenized finance, these firms function as the bridge between traditional capital markets and onchain distribution layers, translating regulated financial products into digitally accessible instruments while preserving the underlying asset integrity and redemption mechanisms.

L2: Tokenization Platforms / Issuers

These platforms turn RWAs into onchain tokens. They work with asset managers to handle issuance, compliance, and ownership records.

For example: Securitize doesn't own the assets, but as transfer agent for BUIDL, Apollo, and Janus, it's the plumbing the institutional giants all route through. Some platforms (Ondo, Maple, Centrifuge) are also issuers in their own right.

In 2025, crypto users' interest in RWAs was largely concentrated around narrative-heavy categories such as tokenized real estate, carbon credits, and diamonds. In 2026, demand has shifted toward more financially structured assets, with activity increasingly concentrated among a smaller set of leading platforms and product verticals:

- Government debt: Ondo Finance, Securitize, Superstate, Centrifuge, STOKR, Spiko Finance, Midas, OpenEden

- Credit funds: Maple Finance

- Home credit: Figure x HastraFi

- Tokenized equities: Ondo Finance, xStocks, Backpack, bStocks

- Pre-IPO markets: PreStocks, Republic (Republic Note), Remora Markets

- Commodities (primarily gold): Tether (Tether Gold), Paxos (Paxos Gold)

Overall, the narrative has matured from experimental, fragmented RWAs into more yield-bearing, institutional-grade financial instruments, with liquidity and issuance increasingly concentrated among established platforms.

L3: Risk Managers / Curators

Risk managers (or curators) are the layer that defines how tokenized RWAs are utilized with DeFi. They sit between asset issuance and capital deployment, translating traditional financial exposure into onchain risk rules.

Their main role is to work with DeFi protocols in setting and maintaining risk parameters such as collateral eligibility, loan-to-value (LTV) ratios, liquidation thresholds, interest rate settings, and exposure limits, to provide curate vaults to end users (liquidity providers).

As RWA adoption grows, more capital is allocated to curator-managed vaults, where users delegate risk decisions to specialized teams rather than managing them directly. This improves capital efficiency while reducing operational complexity for end users.

Top risk managers in TVL include Steakhouse Financial, Gauntlet, Sentora, RockawayX, and KPK.

L4: DeFi Protocols

The beauty of tokenized RWAs is DeFi composability.

DeFi protocols are the execution layer where RWAs become productive onchain capital. Although still early, RWA usage in DeFi has grown from roughly $658M to over $3.2B year-to-date, driven by the integration of private credit, bonds, and structured yield products into money markets.

Key growth has come from RWA collateral being used in lending and yield strategies, including syrupUSDT on Aave via Syrup Finance, JAAA on Centrifuge in Grovedotfinance, syrupUSDC on Morpho, PRIME-related markets on Kamino, reUSD on Pendle, and USTB on Superstate.

A major trend is the rise of RWA collateral in money markets. Users can post RWAs, borrow stablecoins, and retain exposure while unlocking liquidity. Tokenized equities are also emerging as collateral, expanding composability across DeFi. On Solana, Kamino leads RWA lending with close to $941M in active borrow. On Ethereum, Morpho uses a curator model to support RWA collateral like syrupUSDC and mF-ONE, with ~$330M in collateral and ~$240M in active loans generating ~4–7% APY depending on vault risk.

Yield trading turns RWA yield into a tradable asset. The idea is splitting a yield-bearing token into a principal part (PT, redeemable for the face value at maturity) and a yield part (YT, the income until then). Sell the YT, and you've locked a fixed rate. Buy it, and you're speculating on where the yield goes. It's the fixed-income desk of onchain RWAs. Pendle as the best RWA yields in DeFi. Up to 31% fixed APY, locked in at purchase, across gold vaults, insurance underwriting, private credit, preferred shares, and T-bill backed dollars.

Vaults help simplify RWA yield earning. You deposit capital, and vaults allocate it across lending, RWAs, credit, or basis trades depending on market conditions, and distribute yields through yield-bearing tokens. Protocols like Spark, EtherFi, Grove Finance, Huma Finance, Upshift, MulitpliFi, infiniFi, Nest Credit, make institutional-grade yields easier to access.

But the recent collapse of Main Street and Alturax is a reminder that RWA-backed vaults are not risk-free. Insolvency and bank-run risks still exist.

the co-founder of @alturax announced they are winding down the vault.they got hit with a massive withdrawal rush, processing over 8.5 million USDT in just 24 hours.from what I understand the msUSD drama triggered the panic even tho Altura had zero direct exposure to it... Source: MANI

RWA-backed digital money is basically yield-bearing digital dollars with yield coming from tokenized RWAs.

You deposit stablecoins to mint a base dollar and stake it into a wrapper that accrues yield. The return comes from strategies like treasuries or credit markets depending on the issuer.

- Ondo's USDY leads as the largest RWA-backed stablecoin with a total supply of $2.16B, secured by US Treasuries. USDY accrues yield daily, whether you're staking, borrowing, pledging, or just holding it at 3.5% APY.

- Ethena’s USDtb ranks 2nd with over $960M in supply and ~90% of reserves in BlackRock’s BUIDL. You can mint it with USDe on Bybit and used across DeFi money markets like Aave, Euler, Morpho, and Fluid.

- Ethena's USDe is also partly backed by RWAs via Securitize x Centrifuge AAA CLO and Janus Henderson. Ethena is trying to diversify USDe's yield from crypto funding rate into institutional credit yields from AAA CLOs, which are driven by rates and credit spreads instead.

Other RWA-backed digital money that you can hold and earn yields from: USDAI (USD.ai), apxUSD (Apyx), USDf (Falcon Finance), USX (Solstice), ONyc (Onre Finance), USDO (Open Eden),...

L5: Distribution Apps

Distribution apps are the user-facing layer of the RWA stack. They act as the main access point where users interact with tokenized real-world assets, stablecoin yield strategies, and onchain capital markets.

These products include exchanges, crypto wallets, neobanks, and onchain capital allocation apps. Their role is not to design risk or manage assets directly, but to distribute access to strategies built by underlying infrastructure layers such as asset managers, curators, and DeFi protocols.

In practice, they simplify complex financial infrastructure into usable interfaces. Users can deposit funds, earn yield, hold tokenized assets, or allocate capital to different strategies without needing to understand the underlying mechanics such as collateral routing, risk modeling, or vault configuration. The yield and risk decisions are handled upstream, while the apps focus on accessibility, UX, and distribution.

As RWAs mature, these platforms become increasingly important because they determine where liquidity flows. The same underlying yield strategy can scale significantly more when it is integrated into major distribution channels.

Top crypto consumer apps like Coinbase, Binance, MetaMask, Rabby Wallet, Kraken, Backpack, Plasma, Ledger, Bybit, Moonpay and Exodus now offer institutional-grade yield in their products. Tokenized assets are finally made accessible to retail and professional users at scale.

To sum up

Crypto-native tokens are struggling to hold their prices. RWAs are booming.

Ironically, that growth doesn't reflect in the tokenization platforms' tokens, or the chains' native tokens. Most of the value flows to the asset issuers and holders instead.

The tailwinds keep RWAs more attractive than crypto-native tokens:

- Rates stay high. The Fed is holding at 3.5-3.75% and now leaning toward a hike, while the ECB is tightening too. As long as rates stay up, a tokenized T-bill paying ~4% is real yield you can hold onchain.

- Stocks go global. Tokenized equities open US markets and private companies to anyone with a wallet, anywhere, around the clock. We didn't expect this a year ago.

- Stablecoins continue to grow. Every new stablecoin minted effectively routes more dollars into tokenized treasuries. Crypto payment and neobanks drive this trend.

- Capital is rotating. Money is leaving speculative crypto for AI, chips, tech stocks, energy, defense...Tokenization is the bridge that brings them onchain.

- Airdrop. Crypto is fun because of airdrops. As more DeFi builds on tokenized assets, there will be more chances to farm incentives and earn airdrops. The recent RE airdrop gained us some hope back.

However, as the space grows, so do the risks. Synthetic assets, leveraged vaults, and poor risk management can turn innovation into a nightmare.

The opportunity is massive. The challenge is building products that deserve the trust they're attracting.

FAQ

What is RWA tokenization?

RWA tokenization turns a real-world asset — a Treasury bill, a stock, a gram of gold — into a token on a blockchain. The token tracks the real asset's value, not crypto speculation. A tokenized T-bill earns the same ~4% the bond pays; PAXG is backed 1:1 by vaulted gold.

The catch: the token is a claim, not the asset. You're trusting the issuer and custodian to hold the real thing and honor redemptions.

What are examples of RWAs?

The main categories are US Treasuries, private credit, tokenized stocks and ETFs, and commodities (mostly gold). Names: BlackRock's BUIDL and Franklin Templeton's BENJI for treasuries, Maple for credit, Ondo and xStocks for equities, Tether Gold and PAXG for commodities. Stablecoins are technically the largest RWA category but tracked separately.

How do I invest in tokenized RWAs?

Buy them through a self-custodial wallet or a regulated platform. Non-US users can access 400+ Ondo tokenized stocks and ETFs directly in MetaMask, no KYC, in supported regions. Treasury and gold tokens trade on major DEXs and CEXs.

Match the product to your situation: USDY opens to non-US retail for 1 USDC; institutional funds like BUIDL gate at $5,000,000. Verify the contract address before buying.

Are tokenized RWAs safe?

Lower-risk than speculative tokens, not risk-free. You're trusting the issuer, custodian, and redemption process — not just the smart contract. Treasury tokens sit at the safe end; leveraged RWA vaults sit at the risky end.

The 2026 Alturax vault wind-down is the reminder bank-run risk is real. The green flag: proof of reserves plus regular third-party attestation. No attestation, no trust.

How big is the RWA market in 2026?

The tokenized RWA market (excluding stablecoins) is roughly $32 billion as of mid-2026, up from about $5 billion at the start of 2025 — over 4x in 15 months. Add stablecoins and it clears $300 billion.

Standard Chartered projects $2.7 trillion by 2030. Treat that as an analyst bet, not a fact.

I'm building a tokenized RWA protocol. What is the best marketing strategy for RWAs in 2026?

Marketing institutional-grade RWA yield products is a trust sale, not a hype sale. The DeFi marketing playbook of KOLs shilling “high yield” actually backfires here, as it signals to institutional buyers that you may not fully understand your market.

What works instead is a focus on credibility and clarity: creators who can explain your custody setup, oracle design, and legal structure in depth; research content that earns citations and is referenced by others; and a visible, consistent governance presence that demonstrates long-term alignment. Pink Brains KOL Studio matches RWA projects with well-vetted, experienced DeFi influencers who specialize in educational content and protocol analysis, rather than generic promotional threads.

.png)

%201%201.png)