The State of Decentralized AI in 2026

15 mins

A report by Silicon Valley Bank suggests that 40 cents of every $1 in venture capital that went into crypto companies in 2025 also went to firms building AI. A year earlier, that figure was 18 cents. When the smartest allocators in the room reprice that hard, that fast, it usually means the plumbing is shifting underneath the narrative.

Here's the tension driving it. The centralized AI buildout has crossed into genuinely absurd territory - xAI's Colossus cluster chasing a million GPUs, Stargate burning toward 1.2 gigawatts in Texas, GPU shortages hitting more than half of generative-AI companies.

AI creates intelligence, but blockchain creates trust. AI automates decisions, while blockchain makes those decisions verifiable. AI generates value, and blockchain makes it possible for that value to be owned and shared by the people who contribute to creating it.

This is the market breakdown of decentralized AI: what each layer does, why it matters now, the protocols leading it, and where we think it goes through 2026 - 2027.

The Problem: Why AI Needs Blockchain

Decentralized AI exists because centralized AI has structural bottlenecks that capital and code can't fix from inside the walled garden:

- Compute is scarce and expensive

- Control is dangerously concentrated

- Model outputs aren't verifiable

- Training data is getting harder to access

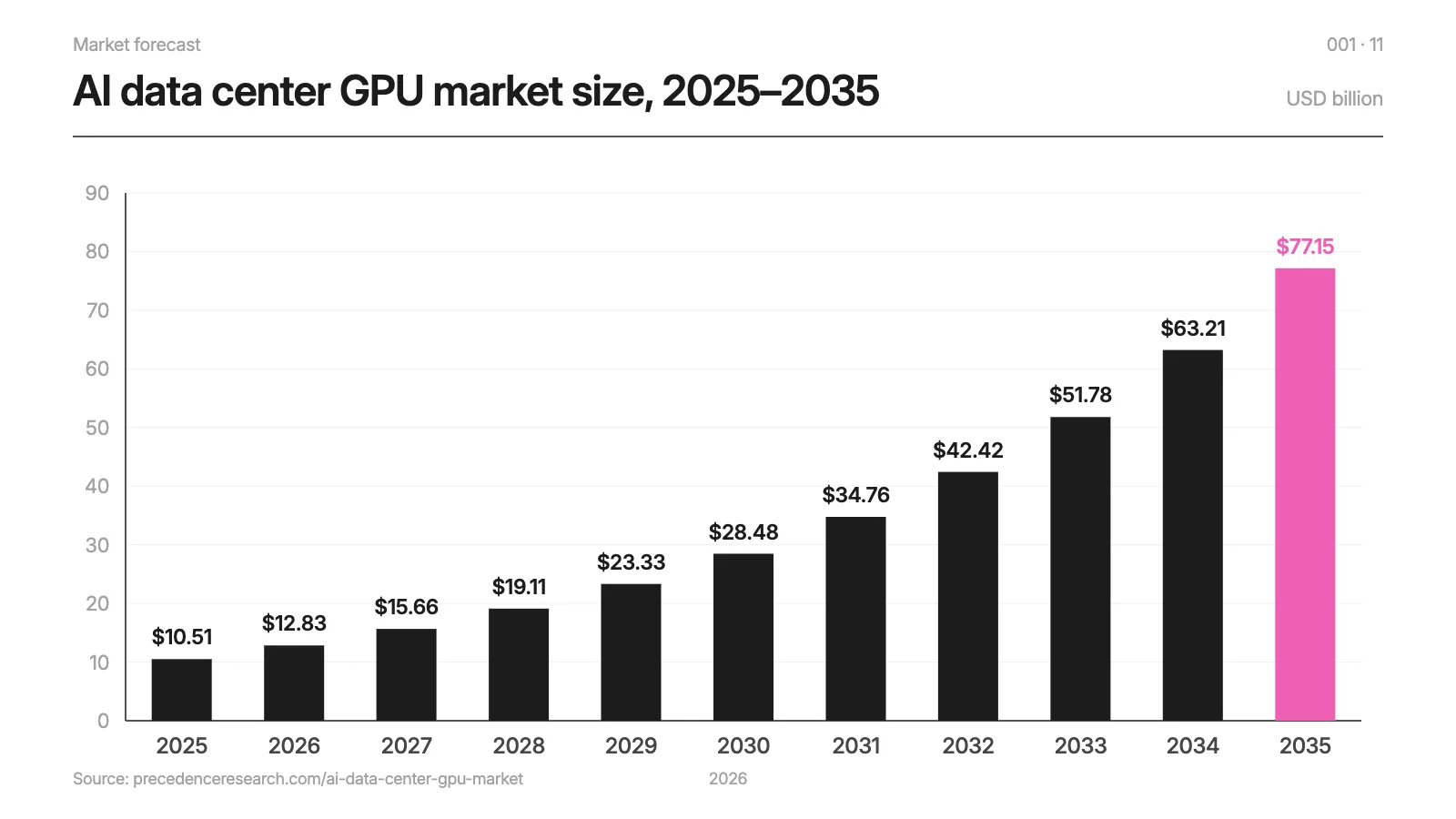

Start with compute and cost. NVIDIA's Jensen Huang said at CES 2026 that AI computation requirements are "increasing by an order of magnitude every single year," and GPU infrastructure is projected to grow from $10B in 2025 to $77B by 2035. Data-center GPUs have been effectively sold out for months at a stretch, which pushes smaller AI teams, researchers, and startups toward alternative supply.

The decentralized compute market is forecast to grow from $9B in 2024 to $22B by 2035 (by Research and Markets) - a number that only makes sense if you believe the shortage is structural, not cyclical. We think it is.

Then there's concentration. Today's most powerful foundation models - ChatGPT, Gemini, Grok, Claude - are owned and operated by a handful of private corporations. That's not just an ideological problem; it's a political-economy one. The entire framework of current AI policy assumes that powerful systems can only be trained by a small number of entities able to amass enormous compute in one place. Break that assumption, and you change who gets to build frontier intelligence at all.

The third gap is verifiability and privacy. AI remains a black box: when a model makes a decision, users often can't verify whether the correct model was run, whether the computation was executed properly, or whether sensitive data was exposed. These concerns become critical when AI is handling loans, financial transactions, healthcare decisions, or autonomous agents with access to sensitive systems.

This has created a growing demand for verifiable and privacy-preserving AI. Instead of relying on corporate policies or trusted operators, the goal is to enforce privacy and accountability through cryptography and code. Technologies like Trusted Execution Environments (TEEs), federated learning, and zero-knowledge machine learning (zkML) aim to make AI systems provably private and verifiable.

The fourth is data access. AI labs are starving for live, geographically diverse public web data, and a centralized scraper sitting in a single AWS region gets rate-limited, geoblocked, or fed a poisoned cache almost instantly. As a16z framed it in its 2026 outlook, data quality and access have become a contested resource, and privacy is becoming "the most important moat in crypto."

AI needs blockchain to make intelligence open, verifiable, and economically accessible.

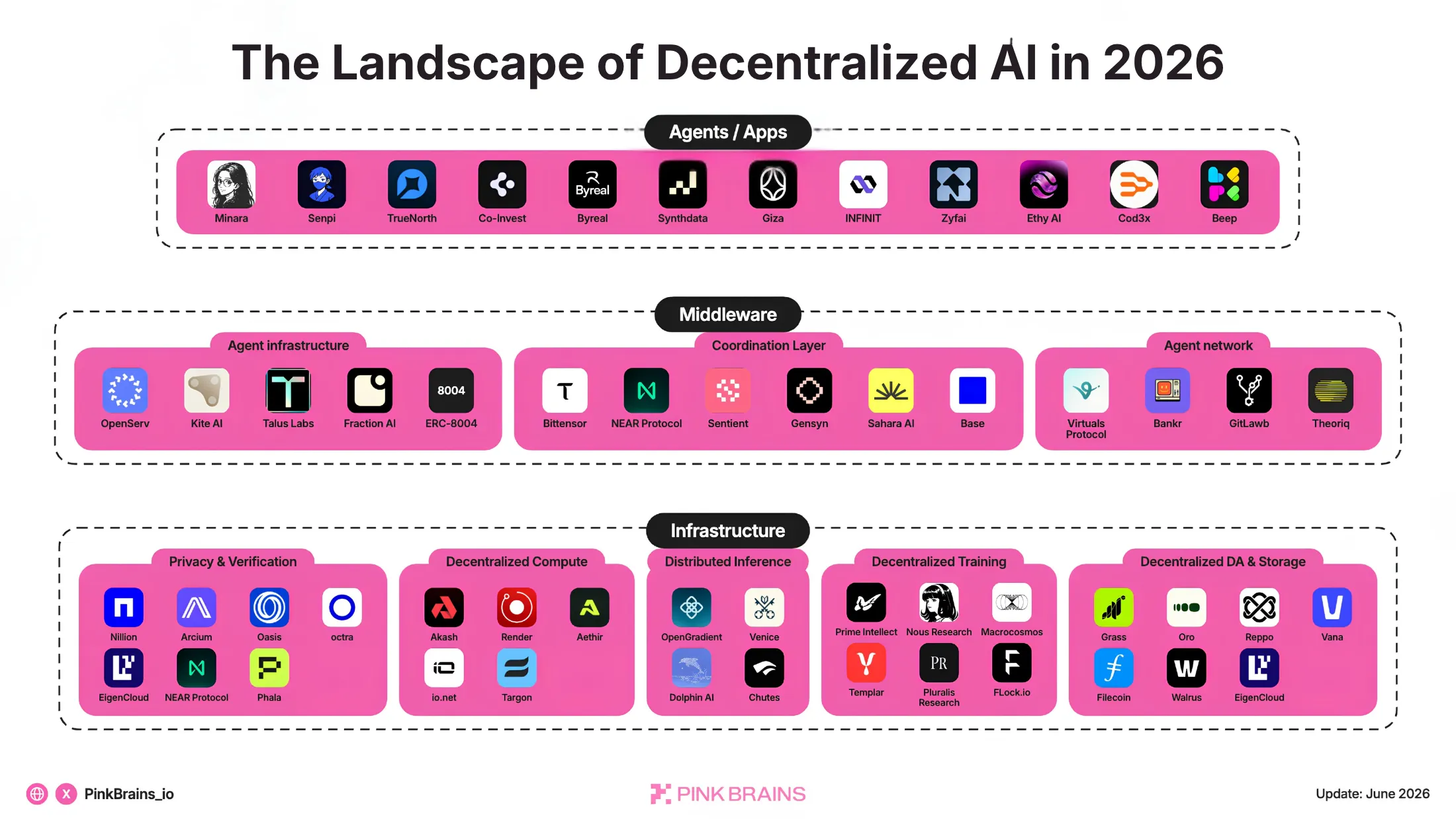

Quick map of the Decentralized AI stack

- Applications & Services: AI agents can do many things, but in crypto, two use cases dominate today: agentic finance and payments

- Middleware: the connective tissue: from frameworks to build and identify agents, agent marketplaces; coordination layers

- Infrastructure: the resources for AI: privacy and verification layer, compute, inference, training, data and storage

The Decentralized AI Landscape 2026

Layer 1: Applications & Services

The application layer is where decentralized AI stops being infrastructure and starts being something a person, or an agent uses.

In 2026, this layer split into three live categories: agentic finance (AI in trading, prediction markets, payment and DeFi), and agentic payments (machines paying machines). With apps running on AI, and AI agents entering the workforce, the agentic economy is being shaped and will continue to boom over the next 3 years.

Agentic Finance: AI trading, prediction markets and DeFi

Most projects in agentic finance focus on turning natural-language prompts into onchain action through interfaces sitting on top of execution venues, increasingly built around top perp DEXs like Hyperliquid for auto-trading, strategy analysis, and Polymarket for prediction trading.

- Minara: Built on Hyperliquid and recently Lighter, Minara runs the full "analysis → decision → execution" loop via its DMind model and 50+ integrations. Recent ecosystem shifts suggest Minara is treating agents as the actual users, fundamentally altering the broker paradigm.

- Senpi: A non-custodial "personal trading agent" for Hyperliquid that started life inside Airstack (the Moxie/Farcaster team), raised a $4M seed, and runs on OpenClaw with progressive autonomy: start with alerts, graduate to letting the agent attach stops and ladder profit targets, eventually hand off whole strategies.

- TrueNorth: Built as a "financial inference layer" backed by CyberFund. It operates on "Agentic Orchestration," moving beyond passive lookup to autonomous portfolio monitoring.

- Co-Invest by Liquid: Puts live trade execution directly inside ChatGPT and Claude across 500+ markets - crypto, equities, FX, prediction markets, pre-IPO secondaries - routing through Hyperliquid, Lighter, and Ostium. By leveraging the Model Context Protocol (MCP), users can execute trades directly within their AI assistants, eliminating the fragmented workflow of legacy dashboards.

- Byreal is the first agent-native DEX on Solana, incubated by Bybit. Its Byreal Perps Agent Skills are the agentic execution layer that gives autonomous AI agents full access to Byreal's CLMM DEX on Solana.

- Cod3x provides a network of lightweight AI agents that turn a plain-language intent ("earn 20% on my USDC at low risk") into built-and-executed onchain transactions, collapsing what'd normally take multiple apps and bridges into one confirmation. It uses RAG + fine-tuned LLMs to parse intent. Its flagship trading agent, Big Tony, runs on Allora's decentralized price-prediction inferences.

On the prediction-market side, Synthdata is the one to know. It's a Bittensor subnet running a decentralized network for predictive financial intelligence. Miners compete to model short-term price uncertainty. It's already feeding live products like Mode's AI Quant on Kalshi crypto markets.

AI agents are also taking part in DeFi - autonomous, non-custodial agents that execute multi-step yield and lending strategies so you don't have to babysit positions across ten protocols. AI is to set to define the next DeFi trend in 2026 and beyond.

- Giza: Its flagship agent ARMA has executed over 100,000 trades and optimized more than $30 million in user capital, operating block-by-block and non-custodially. What makes Giza more reliable is that it's built on EigenLayer's AVS framework - operators stake GIZA to run the decentralized execution layer - and uses smart accounts and session keys so the agent can act within cryptographic guardrails without ever touching your principal. As of March 2026, its agents had processed over $3 billion across selected lending markets. Giza calls the end state "Xenocognitive Finance," which is a mouthful, but the underlying idea is that agents manage capital faster than human cognition allows.

- INFINIT: A "swarm" of 20+ specialized agents (a mindshare agent, a yield agent, an insight agent, execution agents) that translate a plain-language goal, for example, "earn $1,000 monthly on 1 BTC", into one-click multi-step strategies across Ethereum, Solana, and Base.

- Zyfai: A self-custodial DeFAI agent that automates and optimizes yield farming, continuously rebalancing capital across protocols to chase risk-adjusted APY without manual intervention. Two modes: a fully autonomous Agent Vault and a prompt-based mode for hands-on users. Built by the team behind Zyfi, an account-abstraction/Paymaster-as-a-Service infra player from the ZKsync and Base ecosystem.

Agentic Payments: machines paying machines

Just as the internet became the communication layer for the digital economy, blockchain and stablecoins are becoming the settlement layer for agentic payments.

Read our X article on the "Payment Rails for AI Agents".

The breakout is x402 - Coinbase and Cloudflare's open protocol that revives the dormant HTTP 402 "Payment Required" status code, turning any API endpoint into a paywall an AI agent can pay through in stablecoins, no account or credit card required.

The traction is real. As of May 2026, x402 had processed over 173 million transactions on Base and Solana, with the x402 Foundation counting Google, Visa, AWS, Circle, Anthropic, Stripe, and Cloudflare among its members. Stripe began using it in February 2026; AWS launched native AgentCore Payments support in May.

Even with an ecosystem valuation around $7B, x402 has only been processing roughly $20k-$50k in daily volume. Most of this volume settles on Base, which has captured $15.8 million of the $17 million processed since October 2025. Buyer and seller activity is increasing, and most of the transactions are tied to real pay-per-request usage: API calls, AI inference services, agentic commerce and similar workloads. The initial hype cycle has cooled off, but the underlying traction is beginning to catch up.

Meanwhile, Stripe and Tempo's Machine Payments Protocol is emerging as a secondary rail, recording over 411,900 transactions and 9,600 buyers since launch. Together, these networks signal a broader shift toward machine-to-machine commerce, where software agents can transact autonomously at machine speed.

Layer 2: Middleware

As the number of AI agents grows, so does the complexity of coordinating them. Middleware provides the infrastructure for agents to discover one another, exchange services, manage payments, and operate within larger economic networks.

Agent infrastructure

Today's systems weren't built for autonomous agents. Most companies still rely on API keys, while few treat agents as independent identity-bearing entities. Agents can transact, use tools, and interact with other agents, but they lack portable identity, reputation, and accountability.

This trust gap could become a major bottleneck for agentic commerce. Estimates for the market range from $1.5T to $5T by 2030, but consumer adoption remains constrained by a single factor: trust. While many users are comfortable using AI for research, far fewer are willing to let AI make purchases on their behalf.

Blockchain is the ledger for verifiable autonomous systems.

- OpenServ - a full-stack platform for building and operating autonomous AI agents, offering SDKs, agent tooling, generative UI, and crypto-native integrations, with the SERV token used for payments, staking, and governance.

- Kite AI - a purpose-built Layer-1 for the agent economy that makes identity and payments native primitives, anchored by its three-tier Agent Identity Resolution stack (user → agent → session keys) so an agent can transact and be audited without exposing its owner's wallet.

- ERC-8004: an Ethereum standard for "Trustless Agents" that gives agents portable onchain identity, reputation, and validation through three lightweight registries. This lets an agent's track record follow it across chains.

Marketplaces: where agents get launched and owned

- Virtuals Protocol is the biggest operating system for the agent economy on Base. Virtuals provides agents with onchain identity, wallets, payments, compute access, and a framework (ACP) for agents to discover, hire, and transact with one another. It’s also a token launchpad to capitalize AI agents, and is expanding into robotics through Eastworlds. By May 2026, the ecosystem had processed over 2.38M agent jobs and generated nearly $480M in Agentic GDP, with a 10% increase in agentic wallets in the last 30 days.

- Bankr is the social marketplace for agents. Every agent gets a cross-chain wallet, can launch its own token, and can use fee revenue to fund compute costs. Around that, Bankr provides APIs, plugins, marketplaces, and agent-to-agent payments, making it easier for agents to operate as self-sustaining businesses.

- GitLawb extends that idea to code itself: a decentralized git network on Base where repos are "living artifacts. Code written by agents, reviewed by agents, deployed by agents," with Bankr integration letting any repo issue a token tied to its onchain identity.

Coordination layers: organizing decentralized intelligence

Bittensor is the crown jewel of coordination, and it's the most important single network in the middleware layer for AI.

Bittensor is a network of specialized subnets. Each is its own micro-economy where miners run AI models, validators score the outputs, and TAO emissions flow to whoever produces the most useful work. What makes Bittensor economically competitive for decentralized AI coordination is:

- The December 2025 halving cut daily TAO issuance from 7,200 to 3,600 (next halving December 2026, down to 1,800) against a hard 21-million cap.

- The dTAO upgrade gave every subnet its own Alpha token and AMM pool, so the market decides emissions.

- The Taoflow upgrade, live since November 2025, allocates emissions purely by net staking flows - a subnet bleeding more unstakes than stakes can drop to zero emissions. It's Darwinian by design.

The result has been growth across key metrics: more active subnets, more accounts, more TAO staking and allocation to subnets.

- The network crossed 128 active subnets with a combined subnet-token cap that's swung between roughly $1.4 billion and $550 million across the top names depending on the month

- Revenue is showing up. The top 3 compute subnets reportedly hit a combined $20M ARR within three months of monetization.

Others focus on creating dedicated AI blockchains or offering the tools, frameworks, and incentive mechanisms needed to support community-owned AI ecosystems.

- NEAR Protocol: Through Intents and chain abstraction, agents can negotiate, route payments across 35+ chains, and settle transactions using fiat, stablecoins, or crypto. NEAR positions itself as an invisible coordination layer, combining settlement, identity, privacy, TEEs, MPC, and PII protection for autonomous agents.

- Base isn't an AI product itself; it's positioning the L2 as the home base for the "AI agent economy." Base MCP allows AI tools like Claude, ChatGPT, and Cursor execute onchain actions - swaps, transfers, DeFi interactions - via natural-language prompts (non-custodial, OAuth 2.1, launched with Uniswap/Morpho/Moonwell). Its 2026 roadmap commits to "agent-native smart accounts," CLI/MCP access, and the x402 payment protocol for agent-to-agent payments (Coinbase is the top x402 facilitator).

- Sentient: Its GRID ecosystem connects agents, models, data, and compute, routing queries across specialized participants to deliver the best result. The thesis is AGI as a network of collaborating intelligences rather than a single model, with coordination enabled through Sentient Chat, Spaces, and the open-source ROMA framework.

- Gensyn: Rather than a GPU marketplace, Gensyn focuses on verifiable ML execution, coordinating distributed hardware for training and inference while ensuring work can be trusted. Off-chain compute is paired with onchain task assignment, validation, dispute resolution, and rewards, with the AI token coordinating the network.

- Sahara AI: It connects data, models, agents, and rewards within a single AI-native ecosystem. Its Brain-Perceptor-Actor architecture enables agents to collaborate while maintaining onchain provenance, attribution, and automatic value settlement.

Layer 3: Infrastructure

Infrastructure is the skeleton for AI - the raw compute, inference, training, data, and privacy primitives that everything above depends on. This is the most capital-intensive layer, the most revenue-legible, and the one where the "fills the compute gap" thesis is most concrete.

Decentralized Compute

While the AI data center GPU market is projected to reach $77 billion by 2035, the GPU-as-a-Service market is expected to grow to $26B, expanding at a 26.5% CAGR. Businesses increasingly rely on cloud-based GPU resources for scalable AI training, predictive analytics, and real-time data processing. Decentralized compute networks rent out distributed GPU capacity as a cheaper, permissionless alternative to the hyperscalers.

Akash is the cleanest case.

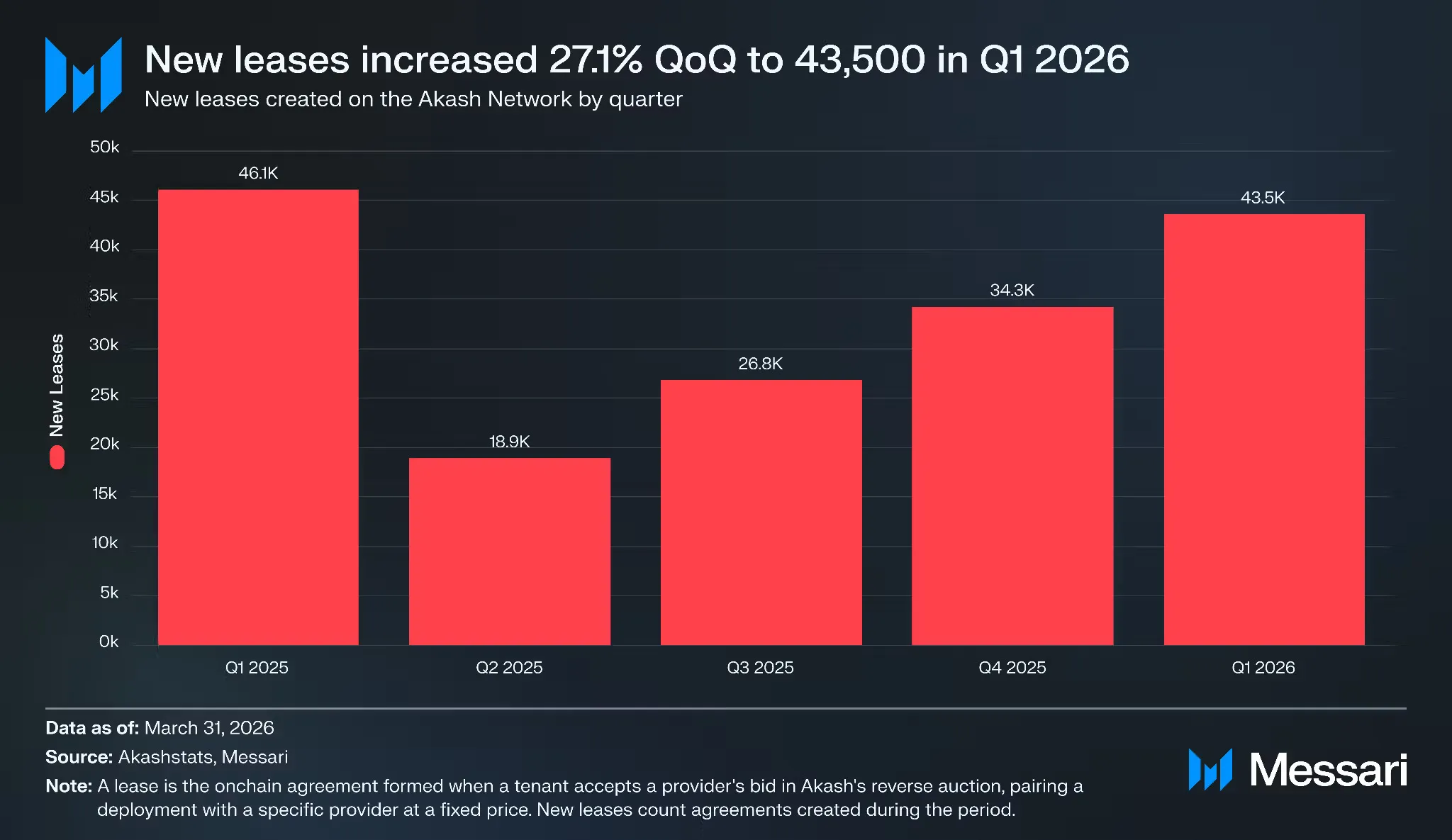

- Akash runs a reverse-auction marketplace - providers bid down to win your workload. Akash recorded 43,500+ new leases in Q1 2026, up 27%, marking the third consecutive quarter of growth.

- AkashML inference service for open-source models like Llama, DeepSeek, Qwen3, processed nearly 120 billion tokens in April alone. By leveraging decentralized GPUs, AkashML AI offers up to 60-85% lower cost than major cloud providers.

- Akash’s Burn-Mint Equilibrium ties AKT tokenomics to real compute demand. Each payment buys and burns AKT while providers receive stable ACT credits.

- Render: pivoting from creative rendering to general-purpose AI compute, Render posted 428% year-over-year usage growth with utilization above 80% and onboarded NVIDIA's Blackwell B200 chips.

- io.net - decentralized GPU cloud on Solana - plays the scale-aggregation game with 130,000+ GPUs across 130+ countries using a Ray-based orchestration layer that makes distributed GPUs behave like a single cloud cluster.

- Targon (Bittensor SN4) - a confidential compute and verification subnet offering secure inference-as-a-service to enterprises, which is the more specialized, privacy-focused end of the compute market, thanks to Intel TDX Trusted Execution Environments.

- Aethir aggregates enterprise-grade GPUs (NVIDIA H100/H200/B200) into a containerized, decentralized GPU-as-a-Service network powering AI training/inference and cloud gaming. It's one of the few crypto-AI infra plays with real revenue: self-reported ~$166M ARR (Q3 2025) and 1.5B+ compute hours delivered. AI agents autonomously booking and paying for GPU inference in real time using its ATH token. Checker Nodes handle uptime verification; Aethir Edge brings consumer hardware into the network.

Distributed and Verifiable Inference

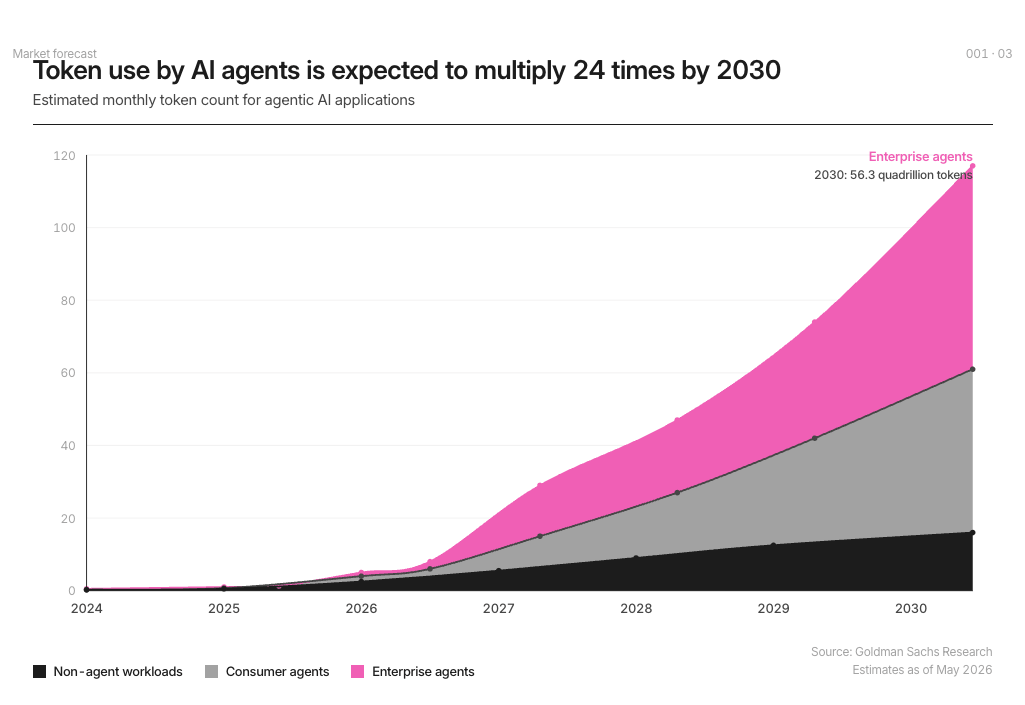

Inference is where models actually run. It is now the biggest cost driver in AI, often accounting for 70%+ of operating expenses. While frontier AI labs are growing revenue quickly, costs are rising even faster due to massive spending on inference and training. Even OpenAI, with 900M+ weekly active users, is reportedly not expected to become profitable until 2029.

Goldman Sachs expects agentic AI to drive a 24x increase in token consumption by 2030, reaching 120 quadrillion tokens per month. Enterprise adoption is expected to become the primary driver of long-term demand.

The next frontier for inference pricing is making that run cheap, private, and distributed with tokenomics and blockchain.

- OpenGradient is a blockchain purposely built for verifiable AI inference, hosts 1,500+ models, and has processed over 2 million verifiable inferences with 500,000+ zkML proofs and TEE attestations. Its $OPG token is the payment rail for verified inference calls.

- Venice has already served 50B+ tokens per day across top text, image, and video models with 2M+ users. Private AI (TEE) and uncensored models are the moat. Dual-token model around VVV staking for DIEM that allows developers to lock in perpetual AI credits ($1 daily credit per DIEM) instead of a subscription, plus a revenue buyback-and-burn.

- Dolphin AI - a decentralized AI inference network. Notably, Dolphin develops the uncensored models used by Venice AI and routes 100% of network revenue into token buybacks. Following its March 2026 migration from DPHN to POD, it remains an emerging but closely watched inference project.

- Chutes (Bittensor SN64) is the serverless option - a decentralized serverless AI compute platform and the highest-emission subnet on Bittensor (~14.4% of emissions). Devs can deploy and scale AI models through simple APIs backed by GPU miners. Chutes is reportedly up to 85% cheaper than AWS, with platform revenue feeding token demand through an auto-staking mechanism.

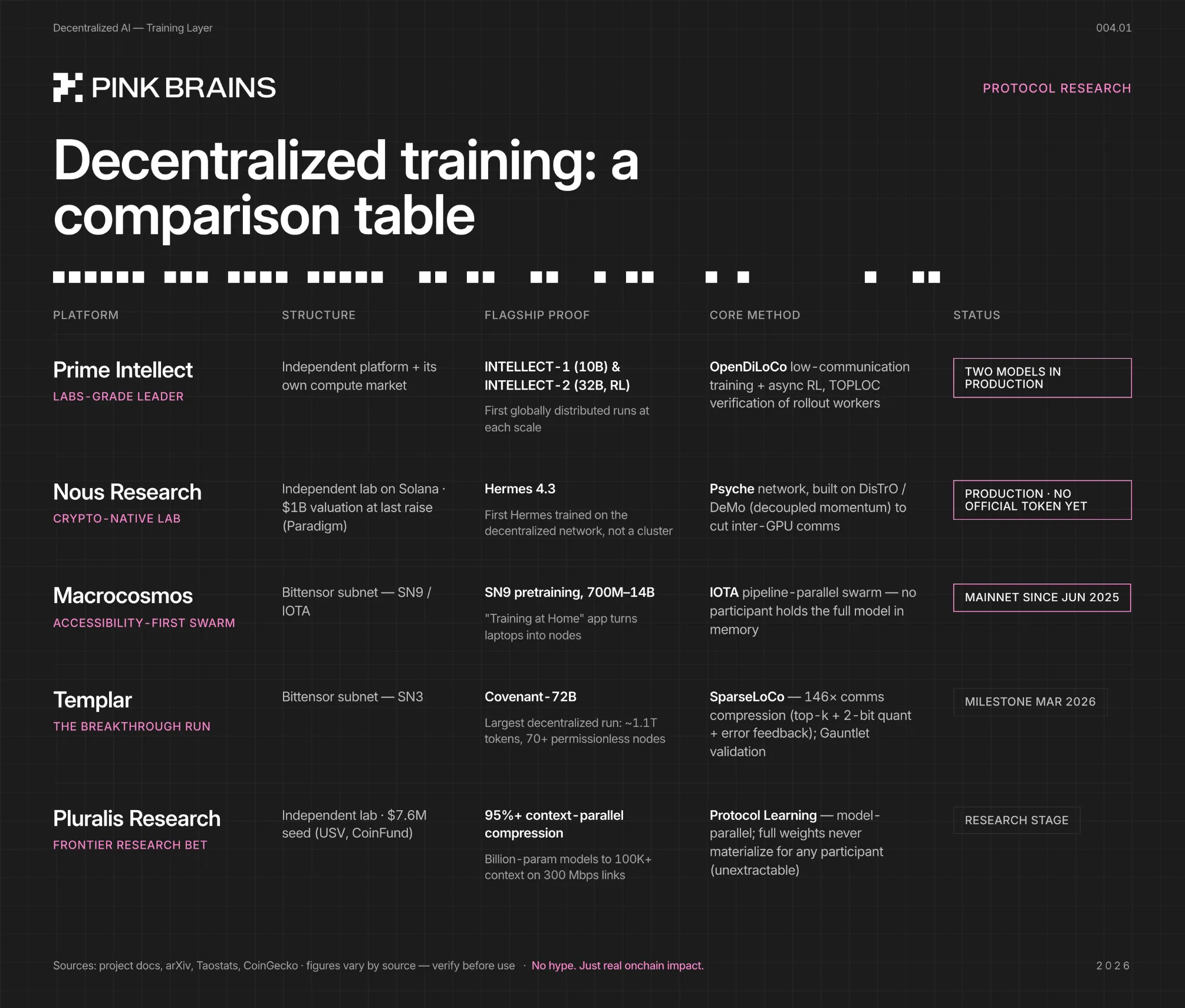

Decentralized Training

Training is the hardest problem in the stack and the one with the biggest long-term implications, because it's the layer that decides whether frontier models must be built inside three or four corporate labs.

- Prime Intellect leads by a clear margin because it shipped. INTELLECT-1 (10B parameters), the first globally distributed training run of its scale, and INTELLECT-2 (32B parameters), the first globally distributed RL training run. Its OpenDiLoCo and asynchronous RL frameworks enable fault-tolerant training across a global GPU network.

- Nous Research raised $50M led by Paradigm, at a billion-dollar valuation. Its Psyche network enables fault-tolerant distributed training, and Hermes 4.3 became the first Hermes model trained on decentralized infrastructure rather than a centralized cluster.

- Macrocosmos operates the training-and-data engine inside Bittensor. Its IOTA subnet (SN9) does decentralized LLM pre-training and "Train at Home," and its Data Universe subnet (SN13) handles the data layer. The enabling breakthrough across all of these is the DiLoCo family of low-communication algorithms, which let GPUs scattered across the planet collaborate without the ultra-fast internal networking a data center provides.

- Templar (Bittensor SN3): achieved one of the biggest breakthroughs in decentralized AI by training Covenant-72B, a 72B-parameter model on ~1.1 trillion tokens across 70+ globally distributed nodes without a centralized cluster. Its SparseLoCo framework reduced communication costs by over 146x, proving large-scale permissionless training is possible, though still behind frontier proprietary models in performance.

- Pluralis Research is developing Protocol Learning, a system that trains frontier-scale models across distributed nodes while ensuring no participant ever possesses the full model weights. This enables collective ownership of models rather than control by a single operator. In 2026, it launched Agora, a pretraining stack that makes consumer GPUs viable for large-scale decentralized model training.

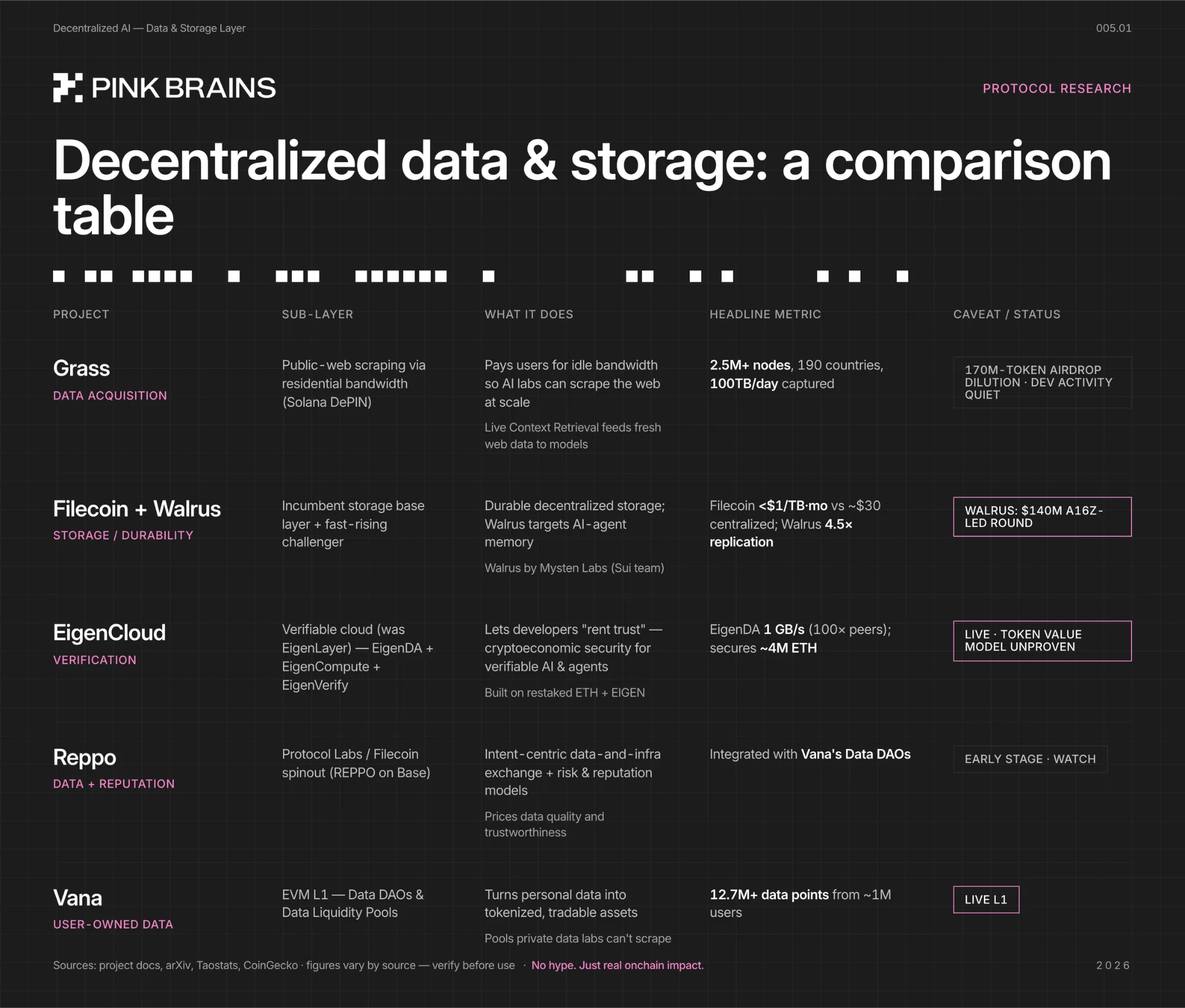

Decentralized Data Availability and Storage

Every layer of the AI stack - training, inference, and agents - depends on two things it cannot generate itself: data and storage.

As AI workloads scale, both are becoming bottlenecks. Frontier models consume massive amounts of fresh data, while storage demand has surged to the point where major hard-drive suppliers report capacity sold out years in advance.

Beyond capacity, trust is becoming equally important. As autonomous agents consume data and act on it, consumers need guarantees that data is private, authentic, and verifiable. This has turned storage from a commodity into a strategic layer spanning data acquisition, durable storage, and data verification while maintaining privacy.

The economics are compelling. Decentralized storage can be 60-80% cheaper than traditional cloud providers, with networks like Filecoin offering storage for under $1 per TB per month versus roughly $30 on centralized alternatives.

- Grass is the data flagship - a Solana-based network paying users for idle residential bandwidth so AI labs can scrape the public web at scale, reporting 2.5 million nodes across 190 countries and 7,000+ TB delivered, with paying clients reportedly including seven-figure AI labs.

- Filecoin remains the incumbent decentralized storage base layer. Walrus is the fast-rising challenger - Mysten Labs' storage and data-availability protocol - using two-dimensional erasure coding to store large "blobs" efficiently, and increasingly positioned as the durable memory layer for AI agents.

- EigenCloud: a verifiable cloud platform built around data availability, verifiable compute, and dispute resolution. Secured by restaked ETH, its thesis is enabling AI agents to operate with cryptographic guarantees, making actions provable, auditable, and enforceable.

- Vana is the user-owned-data network - an EVM L1 where Data DAOs and Data Liquidity Pools turn personal data into tokenized, tradable assets, with 12.7M+ data points contributed by roughly a million users.

- Reppo a data reputation layer focused on evaluating the quality and trustworthiness of AI datasets and infrastructure. It works closely with emerging data marketplaces and Vana’s Data DAOs.

- Oro is a competition for AI shopping agents built on Bittensor. Miners submit shopping agents, validators benchmark them in sandboxed environments using ShoppingBench, and the best performers earn emissions. The real output isn't the leaderboard - it's the high-quality datasets Oro distills into training datasets and shopping-agent models.

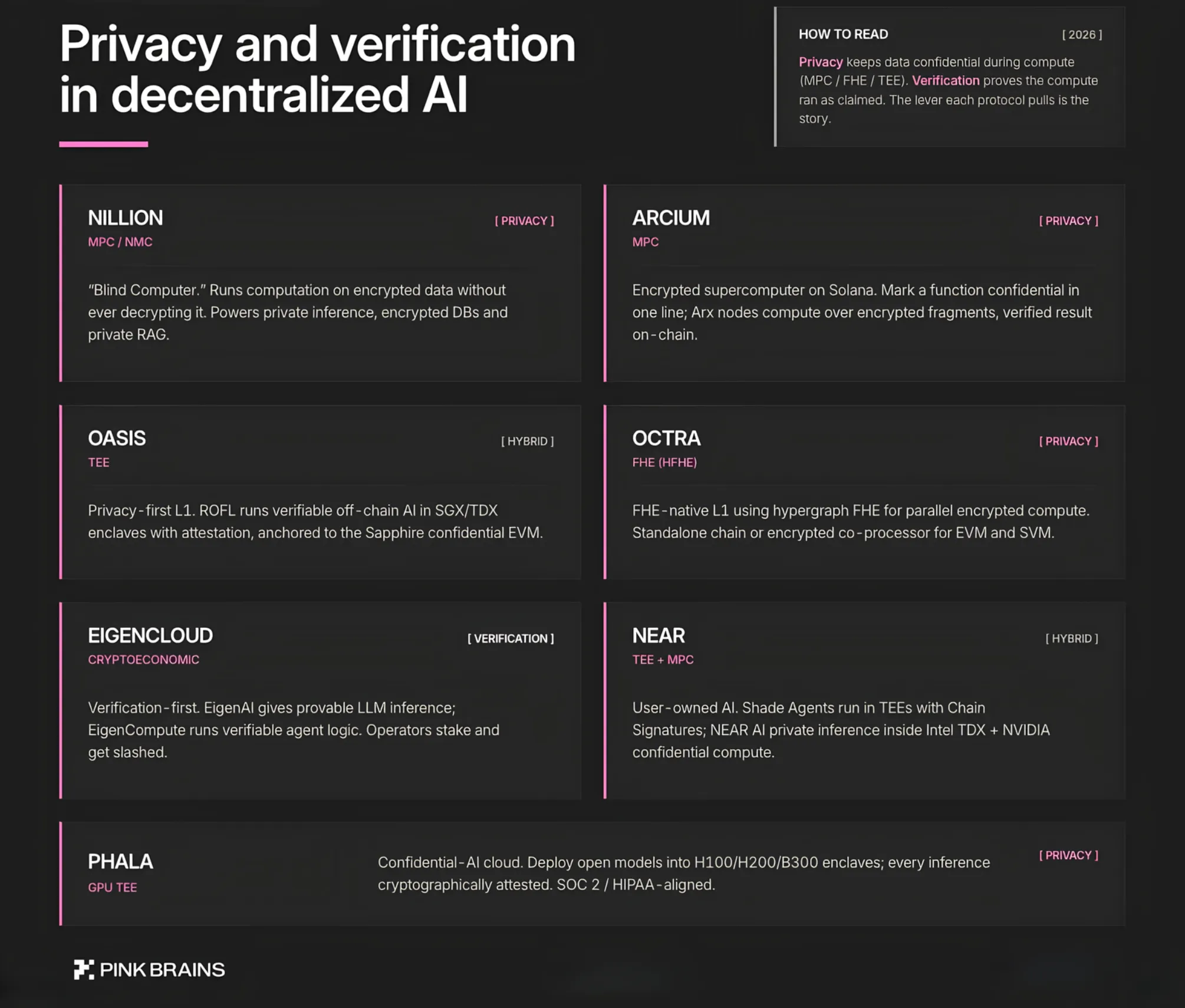

Privacy and Verification Layer

One of AI's biggest challenges is trust. Today, users can't verify that a model handled their data privately, ran the computation correctly, or even used the model it claims to.

This has created a new infrastructure layer focused on two problems: privacy, which protects data during computation using technologies like TEEs, MPC, and FHE; and verification, which proves AI outputs and agent actions are legitimate through cryptography.

The demand is no longer ideological but practical. As AI agents begin managing funds, executing trades, and accessing sensitive information, enterprises and regulated industries need guarantees that data stays private and AI decisions are verifiable. In 2026, privacy and verification are becoming prerequisites for decentralized AI adoption.

- Nillion the "Blind Computer": a decentralized network that performs computation on encrypted data without ever decrypting it, using MPC and its own Nil Message Compute (NMC). The target use cases are private AI inference, encrypted databases, and private RAG (letting an AI query a proprietary knowledge base without leaking it).

- Arcium: A decentralized confidential-computing network ("encrypted supercomputer") built natively for Solana. Developers mark a function as confidential with effectively one line of code; a network of Arx nodes runs it as an MPC computation across encrypted data fragments, then commits a verified result back onchain without exposing inputs. It explicitly positions MPC against FHE (too slow) and TEEs (hardware trust). Live use cases include Umbra (shielded transfers/private yield) and confidential AI training on sensitive datasets.

- Oasis: A privacy-first Layer 1 whose AI play is ROFL (Runtime Offchain Logic), a TEE-based framework for running verifiable, privacy-preserving off-chain compute - AI agents, model training, oracles. ROFL apps run inside Intel SGX/TDX (and increasingly TEE-enabled NVIDIA GPUs), produce a remote attestation, and anchor trust to Oasis's confidential EVM, Sapphire. Its thesis is "verifiable AI with provenance" - proving a model is what it claims and that inference data stayed protected.

- Octra: A privacy-focused L1 native to Fully Homomorphic Encryption, using a proprietary scheme it calls HFHE (Hypergraph FHE) designed for parallel encrypted computation and throughput. It runs as a standalone chain or as an encrypted co-processor / middleware for other networks (including EVM and SVM chains), with isolated execution environments called "Circles."

- EigenCloud: The verification heavyweight, built on EigenLayer's restaking security. EigenAI (verifiable LLM inference is an OpenAI-compatible API for open-source models where prompts and responses are provably unaltered) and EigenCompute (verifiable off-chain execution for agent logic). The model is cryptoeconomic: operators stake collateral and get slashed for delivering unverifiable results, with ZK proofs flagged as a longer-term option.

- Phala positions itself as "the new cloud for confidential AI." Its core product GPU TEE on Phala Cloud deploys open-source models (Llama, Qwen, DeepSeek) into hardware-isolated NVIDIA H100/H200 (and now B300) enclaves, with an OpenAI-compatible API where every inference is cryptographically attested via a "Chat and Verify" tool. Cloud GPUs are powerful but not private; Phala makes the workload provable, shielded even from Phala itself.

Where Decentralized AI Is Heading Through 2026 - 2027

For anyone allocating capital or attention, the question isn't "which token" - it's "which layer compounds." Six vectors define where decentralized AI goes from here.

1. The demand curve is steeper than the prices

The AI-crypto token category sits at roughly $24.6-26.6B and was the best-performing thematic sector in Q1 2026, per Grayscale - down only 14% in the March dip while ~90% of crypto posted losses.

But the underlying market is on a far steeper curve: decentralized AI software is forecast to roughly triple toward $9B+ by the early 2030s, and the broader DePIN shell it rides on - 13M+ contributing devices - is projected by the World Economic Forum to unlock up to $3.5 trillion in economic value by 2028 (value unlocked, not market cap; the sector is still under 0.1% of its trillion-dollar end markets).

2. The agent economy is the clearest growth vector - and the rails are years ahead of the traffic

Juniper Research projects agentic spend rising from ~$8B in 2026 to $1.5 trillion by 2030; McKinsey puts the broader agentic-commerce opportunity at $3-5 trillion by 2030. Onchain today: 17,000+ AI agents, ~4.5M daily active agent wallets, and agent wallets already 8–12% of EVM DeFi transaction volume.

AI-agent transactions are still only ~0.0001% of the $46 trillion in annual stablecoin settlement. That's not a demand problem - it's infrastructure laid ahead of adoption. The 2026-2027 window is the inflection where the rails mature while the traffic is still forming, which is exactly when positioning matters.

3. Onchain markets become the financialization layer for computing power

The most underrated tailwind: AI hardware carries a ~$490B financing gap banks won't underwrite because they can't price a GPU fleet.

InfraFi protocols like USD.AI bridge it. GPU-collateralized synthetic dollars with real legal scaffolding (Delaware SPVs, UCC-1 liens), $1.2B+ in approved facilities, paying 13-17%. When on-chain liquidity finances the physical layer of AI faster than a bank can, the stack gets a funding flywheel centralized AI's balance-sheet model can't match.

4. Institutional rails are arriving - both equity-style and credit-style

Grayscale filed its Bittensor Trust (GTAO) S-1/A in April 2026, intends to list on NYSE Arca as an ETF, and built in staking. Public companies have established TAO treasuries; funds like Yuma Asset Management are launching subnet-focused vehicles.

a16z's 2026 outlook names privacy "the most important moat in crypto," directly tailwind-driving the verifiable-inference and data layers. The category is crossing from retail-narrative trading into institutionally fundable infrastructure.

As GPUs become one of the scarcest resources in the AI economy, financial markets are beginning to adapt. Industry participants expect GPU-bonded futures to launch later this year, while major banks such as Goldman Sachs and JPMorgan are exploring derivatives tied to compute and GPU rental costs as new tools for financing and risk management in AI infrastructure.

5. Tokenomics is the value-capture moat centralized AI structurally cannot copy.

OpenAI's revenue accrues to OpenAI's cap table; a decentralized network's can accrue to the people supplying compute, data, and models - via buyback-and-burn tied to usage (Akash burns $0.85 of AKT per $1 spent; Render burns against 69M+ cumulative renders; NEAR routes Intents fees into $NEAR buybacks; Venice runs a monthly burn), revenue-sharing to supply-side participants, and staking that grants real capacity (Venice's staked VVV mints DIEM, each worth $1/day of inference).

The counter-case worth pricing in: value may instead accrue to settlement rails (Circle, Tether, Coinbase, Stripe, Visa, etc.) rather than the protocols routing through them, the way TCP/IP captured no rents while Cloudflare and AWS did.

6. The category widens from AI into robotics and physical AI (DePAI)

This is the strongest extension story into 2027. Coined by Messari after NVIDIA's "Physical AI" framing at CES, DePAI sits at the intersection of AI, robotics, Web3, and DePIN - and robots need exactly what crypto crowdsources: real-world training data, cheap distributed compute, and ownership incentives. NVIDIA open-sourcing the GR00T humanoid foundation model was the catalyst.

Morgan Stanley sees humanoid robotics at up to $4.7T in annual revenue by 2050. Names already live: GEODNET (19,500+ base stations supplying centimeter-accurate positioning to robots and AVs), XMAQUINA (DAO exposure to private humanoid firms like Apptronik and 1X), and NATIX (decentralized real-world data capture). The same playbook that coordinated GPUs is now pointing at machines.

.webp)

Conclusion

Decentralized AI in 2026 is a multi-layer stack spanning infrastructure, middleware (coordination, identity, marketplace, framework), and apps/agents. Real traction is emerging across the ecosystem - from millions in compute revenue and growing agent economies to large-scale decentralized model training.

But the sector is still early. Revenue often trails token incentives, adoption remains uneven, and while overall AI investment is surging, decentralized AI still captures only a small share of venture capital. Token-driven networks can be a powerful advantage, but only if value accrual is designed correctly.

Even so, the emergence of projects like Bittensor, NEAR, Virtuals, Base, and Venice suggests that decentralized AI is evolving beyond a speculative narrative into a new model for coordinating compute, data, capital, and intelligence.

FAQ

What is the decentralized AI stack in 2026? The decentralized AI stack is the layered set of crypto-AI protocols spanning applications (agentic trading, AI-in-DeFi, agent payments), middleware (agent marketplaces and coordination networks like Bittensor), and infrastructure (compute, inference, training, data, and identity). Each layer provides a permissionless, verifiable alternative to a centralized AI bottleneck.

Which decentralized AI projects are leading in 2026? By category: Akash, Render, and io.net lead decentralized compute; Bittensor leads coordination; Virtuals leads agent marketplaces; Prime Intellect and Nous Research lead distributed training; Grass, Vana, and Walrus lead data and storage; and OpenGradient and Venice lead verifiable and private inference.

Why does AI need blockchain at all? Blockchain addresses four specific AI bottlenecks: it coordinates distributed GPU supply to ease compute scarcity, it decentralizes control away from a few corporate labs, it enables verifiable inference so AI outputs can be cryptographically trusted, and it creates incentive systems for sourcing training data. It's infrastructure for AI's gaps, not a replacement for AI.

Are AI agent tokens a good investment in 2026? They're the highest-risk, highest-volatility part of the sector. Virtuals' VIRTUAL token round-tripped from over $5 to under $1, and many agent tokens trade on narrative rather than usage. Most research desks frame AI tokens as a small, speculative slice of a diversified position rather than a concentrated bet.

What is agentic payments and why does x402 matter? Agentic payments let AI agents pay each other autonomously without human approval. x402, built by Coinbase and Cloudflare, turns any API into a stablecoin paywall agents can pay through, and is backed by Google, Visa, AWS, Circle, and Stripe. It matters as the settlement rail for the agent economy — though real usage still lags far behind its valuation.

Can AI models really be trained without a centralized data center? Yes. Prime Intellect trained a 10-billion-parameter model across five countries, Bittensor's Templar subnet finished a 72-billion-parameter model with no central cluster, and 0G Labs has pushed the technique to 107 billion parameters. Low-communication algorithms like DiLoCo make globally distributed training viable, though the largest fully decentralized runs still trail centralized frontier labs.

.png)

%201%201.png)